Insolvent Trading: A Practical Guide for SME Directors

Understand insolvent trading & its impact on SMEs. Protect yourself as a director or creditor facing insolvency. Learn to trade while insolvent lawfully.

What is an insolvent trading claim?

An insolvent trading claim is an action for breach of a director’s duties. The prohibition against insolvent trading is a duty of all company directors that is set out in section 588G of the Corporations Act. It is a cause of action that liquidators have against company directors after a company is placed in liquidation to compensate creditors.

Sometimes people talk about a director being liable for trading while insolvent. But this is not technically correct. Only a company, not a director, can trade while insolvent. The duty of directors is to prevent that insolvent trading from occurring.

Breaching this duty makes a director liable for a civil penalty for insolvent trading. If, in addition to satisfying the criteria set out above, the director was also dishonest, under section 588G(3) that director may be prosecuted for a criminal offence. ‘Director’ here refers to de facto and shadow directors, as well as de jure directors.

Before the safe harbour protection was introduced in 2017, and the creation of the Restructuring regime for small businesses in 2021, Australia had one of the strictest insolvent trading prohibitions in the world for small-to-medium sized company directors. The law effectively mandated directors to move to external administration as soon as their company was insolvent to avoid risk of personal liability (i.e. being sued by a subsequently appointed liquidator).

What are the elements of an insolvent trading claim?

To establish an insolvent trading claim under section 588G of the Corporations Act 2001, a liquidator must prove each of the following elements:

- The person was a director of the company at the time the debt was incurred;

- The company was insolvent when the debt was incurred — meaning actual insolvency (an enduring inability to pay debts as they fall due or a chronic shortage of working capital), not mere temporary cashflow difficulties;

- The company incurred a debt at that time (the director caused, permitted or failed to prevent the incurring of that debt);

- The director had reasonable grounds to suspect, or ought to have been aware, that the company was insolvent — i.e. a reasonably diligent director in the same position would have formed such a suspicion.

What are the penalties for insolvent trading?

- Civil penalties up to $1.65m

- Liability to compensate the company or relevant creditors for the amount of the debt incurred as a result of the breach

- Disqualification from being a director in Australia

- Potential criminal investigation and prosecution by ASIC where there is dishonesty and the penalty carries 2,000 penalty units and/or up to 5 years’ imprisonment

Essentially, it is illegal for a director of a company to allow an insolvent company to continue to trade, while having reasonable grounds for suspecting insolvency. The consequences can be serious. In a New Zealand case in 2019, Dame Jenny Shipley, former Prime Minister of New Zealand, was ordered to pay $6 million for allowing the construction company Mainzeal to continue trading while insolvent.

What is the difference between civil and criminal insolvent trading?

As discussed above, there are three possible penalties for insolvent trading. Directors may receive, one, two, three or all four penalties, depending on the nature and scale of the insolvent trading and the discretionary decisions of the investigators.

Civil proceedings (bearing the penalties of fines and compensation) are usually pursued first and more commonly in insolvent trading cases, as they deal with recovery of money through the liquidation process.

However, where an element of dishonesty is involved and can be proved, criminal charges may be pursued. It is more likely that a criminal case will be made out where the insolvent trading is especially serious, sustained, relates to high values of money, or is accompanied by other wrongdoing (i.e. accounting fraud, phoenix activity or breaches of other directors’ duties). ASIC is the body in charge of pursuing criminal charges against directors.

Where criminal charges can be made out by ASIC, directors can be fined up to 2,000 penalty units or be imprisoned for up to five years, or both. If a director is found guilty of criminal insolvent trading, they could be permanently disqualified as a director.

When is a debt incurred?

It is important to understand what exactly is meant by ‘incurring a debt’ in the legislation.

The term debt has been interpreted widely for insolvent trading and can include contingent debts. Transactions which give rise to a debt may include supplying goods and services, issuing a loan, entering a lease or guarantee and certain transactions which incur tax obligations (e.g. hiring new staff leads to payroll tax liability).

The legislation also provides that a company has incurred debt when it pays a divided, makes a capital reduction, redeems preference shares, assists an individual to acquire shares or enters into an uncommercial transaction.

Broadly speaking, a debt is incurred if a company, through its conduct, subjects itself to a conditional but inevitable obligation to pay money. ‘Incurring a debt’ is considered in a logical way by courts with regard to commercial reality and the overall purpose of the prohibition on insolvent trading.

Directors of small-to-medium enterprises act differently to large corporate directors

Insolvent trading occurs when a company continues to incur debts while it is unable to pay its existing debts as and when they fall due. To bring an insolvent trading claim, a liquidator must first be appointed and then have sufficient funds—either from the company’s assets or from external sources—to investigate, prepare and run litigation. Empirical evidence shows that relatively few insolvent trading claims are actually pursued to court. The main reasons are practical: litigation is expensive, time-consuming and uncertain, and liquidators often prioritise actions that will yield the greatest return or which receive siginificant financial support from creditors.

Because of these cost and resource constraints, liquidators are less likely to commence proceedings against directors of small and medium-sized enterprises (SMEs) in routine cases, and instead focus on the most serious or clear-cut examples of insolvent trading.

Directors can take practical steps to reduce the risk of allegations of insolvent trading. Two important mechanisms in Australia are the safe harbour and the Small Business Restructuring (SBR) pathway. The safe harbour is a legal defence that shields directors from insolvent trading liability if they can show they were taking a course of action reasonably likely to lead to a better outcome for the company, and that they were obtaining appropriate advice and keeping adequate records. The SBR pathway is a formal restructuring process designed to help eligible small businesses restructure their debts and continue operating, with defined procedures and protections that can reduce the prospect of creditors pursuing insolvent trading claims.

Practical steps directors should consider include: obtaining timely and documented financial and restructuring advice, keeping contemporaneous records of decisions and cashflow forecasts, ceasing to incur new debts if insolvency is imminent, engaging with creditors and exploring formal restructuring options such as SBR, and seeking external advice early if cashflow problems emerge. These measures both lower the practical risk of insolvent trading and improve the director’s ability to rely on defences such as safe harbour if the company later enters liquidation.

What does empirical research tell us about insolvent trading claims?

Academic commentary is not very useful overall for directors because the academic articles that seek to critically analyse insolvent trading want to change director behaviour through policy. Empirical research, which makes a direct observation about insolvent trading in Australia would be very useful. Unfortunately, in Australia there is very sparse empirical research into SME insolvency.

What empirical research is available, however, tells us that liquidators very rarely actually commence insolvent trading claims and run these proceedings to judgment. There is no empirical research into how many letters of demand are sent out by liquidators to company directors, however. This means that we also have no idea what proportion of potential claims are settled out of Court, giving directors and advisors little tangible evidence to help guide the best to approach.

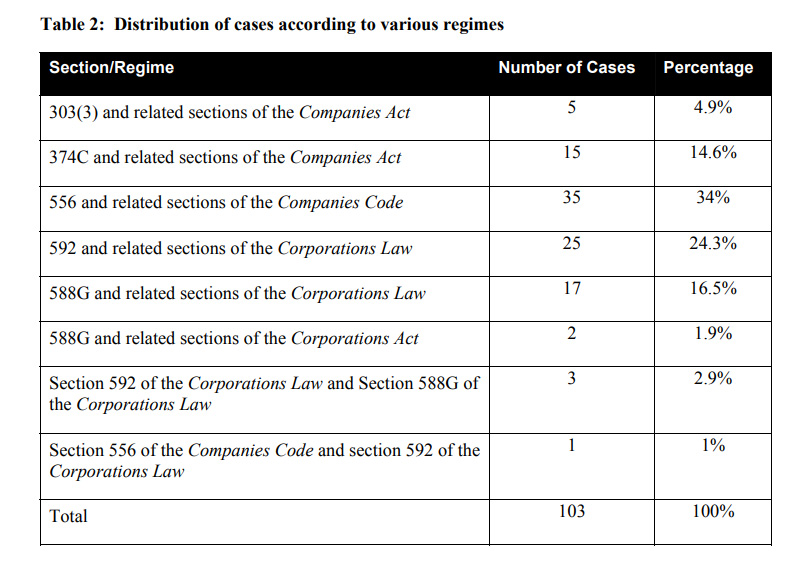

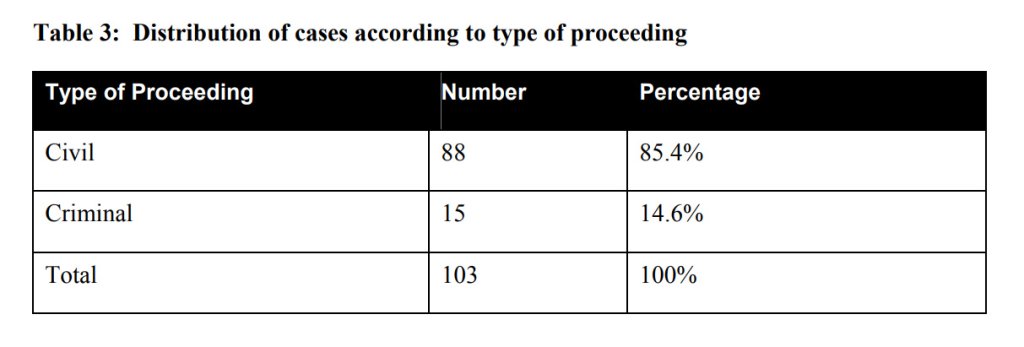

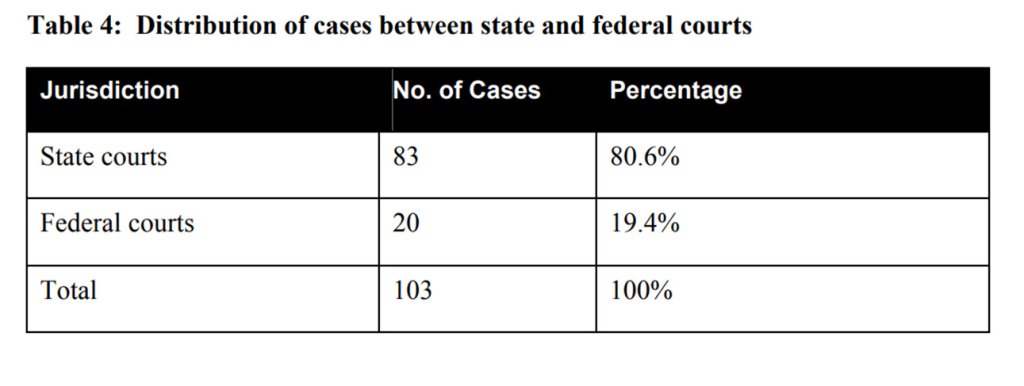

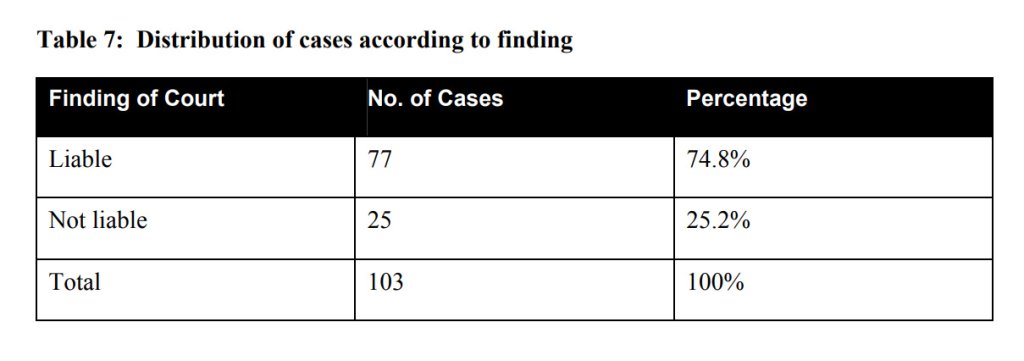

Empirical research conducted by James, Ramsay and Siva (in a collaboration between the University of Melbourne and Clayton Utz) found only 103 cases of insolvent trading brought to court between the introduction of the prohibition in the 1960s and 2004. This is an extraordinary statistic when you consider the number of companies that would have been placed into insolvent liquidation. The chances are not quite one in a million but the chances of being sued for insolvent trading in Australia must be close to negligible. It is therefore very unlikely that a director of an SME (up to 200 employees) would face an insolvent trading action. It is a demanding and expensive exercise for a liquidator to run an insolvent trading claim, so they are usually averse to this course of action unless the debts incurred are significant or they go hand in hand with other wrongdoing.

The following tables from the University of Melbourne and Clayton Utz study reveal important information about insolvent trading cases that proceeded to judgment in Australia.

Table 2 shows the distribution of cases according to which section of which regime they were brought under (please note that the Corporations Act is the current law).

Table 3 shows the distribution of cases according to the nature of the proceeding (i.e. civil or criminal).

Table 4 shows the distribution of cases between state and federal courts.

Table 7 shows the distribution of cases according to whether directors were found liable or not liable for insolvent trading.

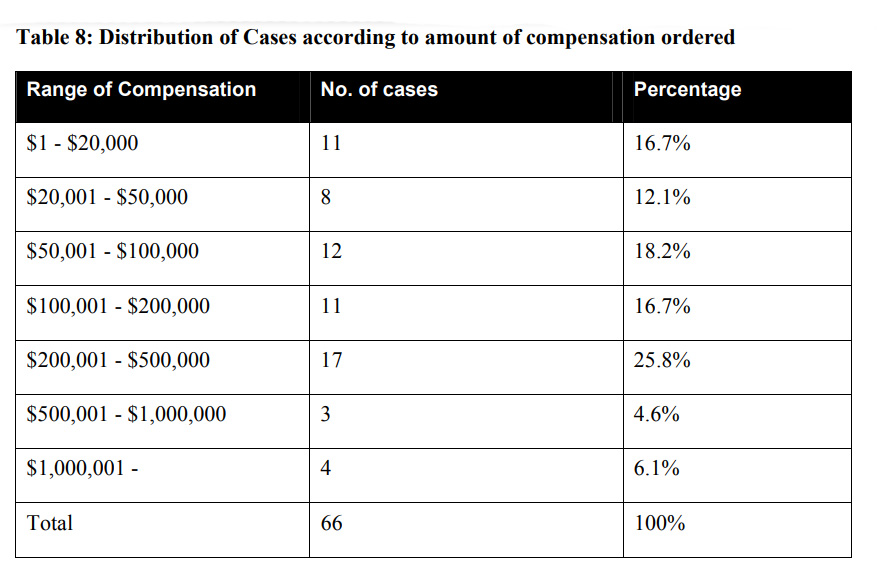

Table 8 shows the distribution of cases according to the amount of compensation ordered.

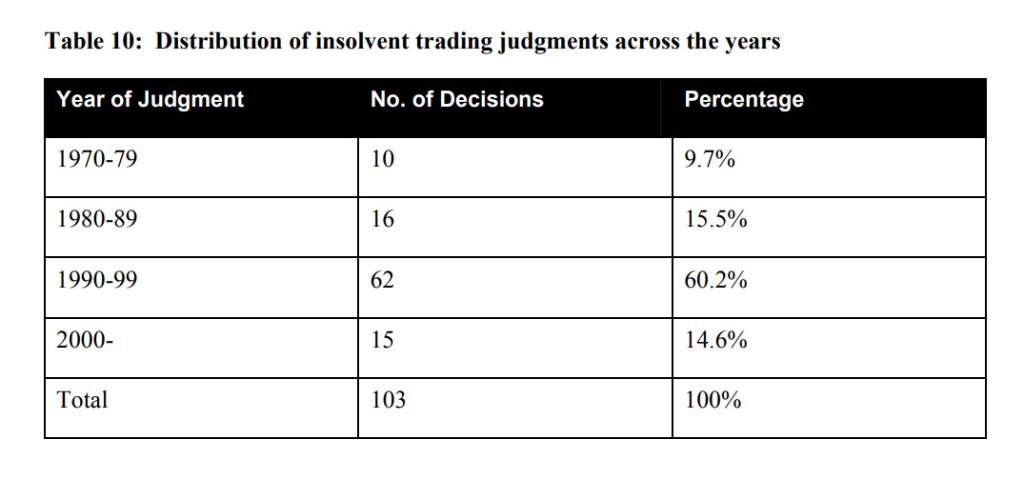

Table 10 shows the distribution of judgments across the years. Please note this study was published in 2004 and only accounts for cases up to and including that year.

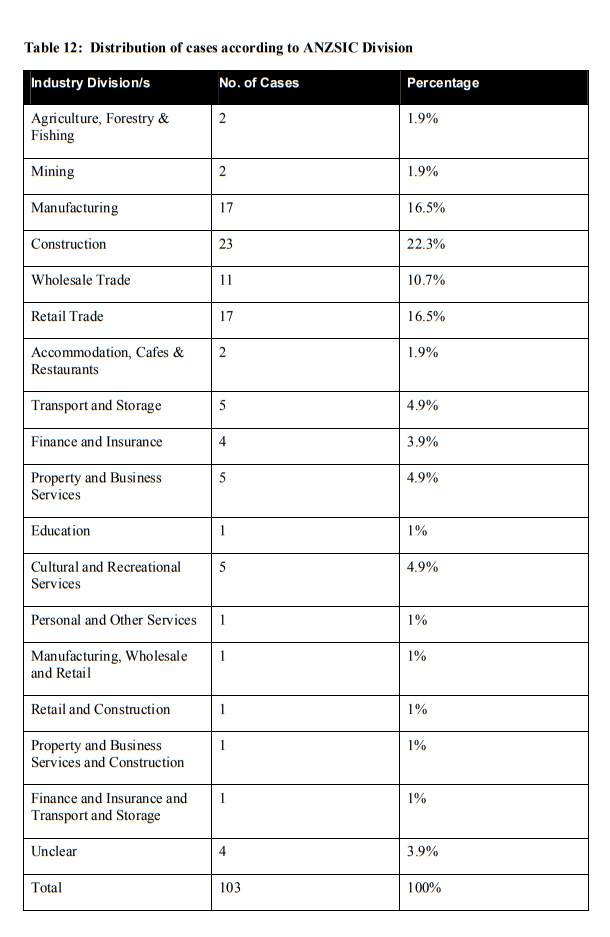

Table 12 shows the distribution of cases according to industry.

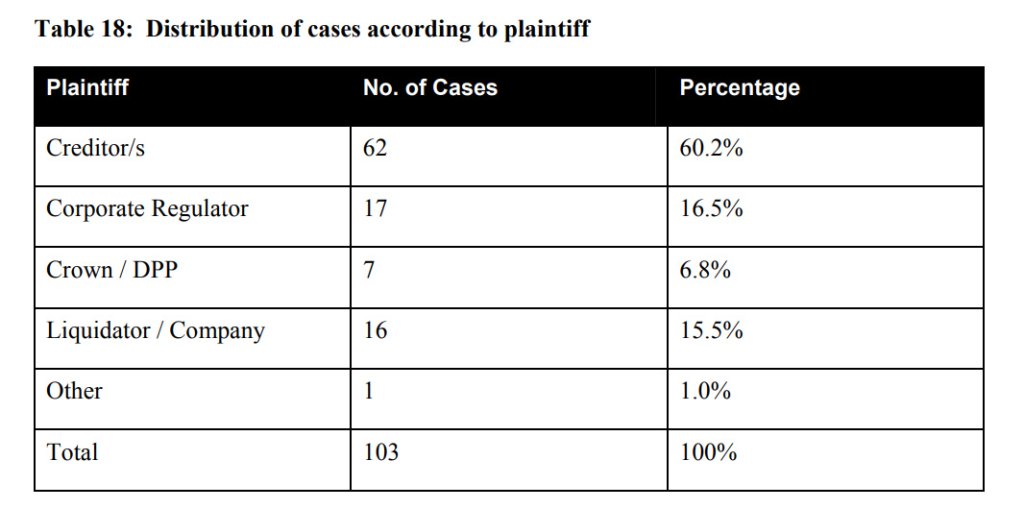

Table 18 shows the distribution of cases according to the nature of the plaintiff (i.e. who initiated the insolvent trading claim).

The above data gives useful insights into the nature of insolvent trading claims, but leaves many questions about how this may have changed or evolved over the last 21 years to 2025. From what the data suggests about trends, and what we have observed within the practice space, we know this: an insolvent trading claim is like a lightning strike: they are rare, but they can be very dangerous if you’re unlucky enough to receive one.

What is the rationale behind the prohibition on insolvent trading?

The prohibition on insolvent trading exists to discourage directors from mismanaging funds. It aims to stop creditor losses from occurring, and to prevent the diversion of economic resources away from the most profitable businesses and operations. Essentially, it operates to stop businesses from incurring further debt when they are already insolvent and will likely cease trading, thus protecting commercial players.

Historically, Australian law has included some form of liability in relation to insolvency since the 1930s (initially focused on fraudulent trading). The first incarnation of the prohibition on insolvent trading was introduced in the 1960s. The positive duty on directors to avoid trading while insolvent was first established in 1993, following a comprehensive review of Australia’s corporate and personal insolvency regime. The review was prompted by the changing social and economic environment in light of Australia’s tenuous economic situation in the early 80s, simplified access to credit, high levels of unemployment and fluctuating interest rates, all of which were perceived to be having an impact on the increase in insolvency proceedings.

Knowing what prompted the review and thus the reforms can help us understand why Australia has some of the strictest insolvent trading provisions in the world, which many refer to as ‘draconian’ and ‘anti-business’. The provision was interestingly not intended to be a punishment for directors, but to provide more opportunities for recourse for unsecured creditors where directors had been reckless.

Below are some of the economic risks that the prohibition attempts to address.

Risk one: Premature insolvency proceedings

Those who oppose the prohibition on insolvent trading argue that it results in directors putting companies into external administration too quickly rather than encouraging directors to take sensible steps to rescue the business. The actual risk of an insolvent trading claim is low but the prohibition itself has a salutary effect, simply because most people want to follow the law.

The downside is that all the goodwill value in a business is lost in liquidation and it is also unlikely that there would be a significant return to creditors.

Risk two: Flogging a dead horse

A business must be sustainable and this means that whatever it produces must be sold for a higher price than it costs to produce. If the business can’t do this then there is no hope for it and the economic resources it utilises should be passed on to more efficient enterprises.

The entire rationale for a prohibition on insolvent trading is to protect creditors. If a company is a “dead horse” then wasting assets through continued trading (that would be available in liquidation to pay creditor claims) should be prohibited.

Risk three: Prognostication and procrastination

Directors of insolvent SMEs usually have imperfect information systems and limited or no access to high quality advisers. That creates a perfect storm for procrastination. They could be stuck at a point of indecision because there is no readily accepted template for how they should behave when faced with insolvency. If they don’t have up-to-date financial information how can they make sensible financial decisions?

Who is going to help? Their accountant and solicitor probably don’t have the inclination or expertise to assist. They may be worried about getting paid for providing services when their client is potentially unable to pay for their fees.

What are the elements of the liquidator’s decision to commence an insolvent trading claim?

Key element 1: Cash at the bank or a funder

Liquidators run professional practices and must recover their fees for the work they perform. Because many liquidations are assetless, there are often no funds available to cover the legal and accounting costs associated with insolvent trading claims. A liquidator cannot be required by creditors to pursue an insolvent trading action where there is no realistic prospect of payment to fund the process. Engaging barristers and instructing solicitors is expensive, so pursuing such claims generally requires a reasonable expectation of recoverable assets.

The alternative if a liquidation is assetless is to seek funding from a creditor or a litigation funder. The game-changer in the insolvency industry is that in the last decade the Australian Tax Office, Department of Employment & Workplace Relations (FEG) and litigation funders have been more active. Having pointed that out, those industry players aren’t likely to be interested in claims that aren’t significant. What “significant” means is changing over time but it is likely to be in the multiples of millions in size. The ATO and FEG have strong policy incentives to pursue the worst cases of insolvent trading and phoenix activity, where debts incurred amount in the tens of millions.

Key element 2: Availability of books and records

When pursuing an insolvent trading claim, the liquidator bears the primary burden of proving the company was insolvent at the relevant times. In practice this often requires careful examination of the company’s books and records: without reliable financial records, a liquidator may lack the evidentiary foundation to commence proceedings. Conversely, directors can rebut allegations by producing contemporaneous records showing the company was solvent when the disputed transactions occurred.

Because insolvency is a fact-specific question, outcomes in insolvent trading cases depend heavily on the documentary and testimonial evidence available. Directors are typically best placed to explain the company’s financial position and the business reasons for incurring debts.

Importantly, the law also treats failure to keep proper books and records as indicative of insolvency—section 588E of the Corporations Act creates a presumption of insolvency where directors do not maintain adequate records, shifting the evidential burden onto them to prove solvency.

Key element 3: Quantum of the claim

Liquidators typically charge high hourly rates and are unlikely to initiate litigation for low-value claims related to insolvent trading; because of the time and expense involved, they generally pursue matters where potential recoveries are substantial—often in the millions—rather than disputes worth only thousands. There is limited research quantifying the likelihood of liquidators pursuing or succeeding in such cases, but practical experience shows a clear preference for higher-quantum claims.

Key element 4: Defendant’s capacity to pay a judgment

Before commencing commercial litigation for insolvent trading, a liquidator will first assess whether the potential defendant can satisfy a judgment. While certain private financial details—such as ASX shareholdings, investment account balances and bank statements—may be inaccessible, liquidators can rely on public records (RP data) and statutory searches. A targeted property search to identify any real estate owned by a director is particularly important: discovered real property, its location and encumbrances materially influence the cost–benefit analysis and the decision to pursue insolvent trading proceedings. This preliminary assessment helps determine whether litigation is viable and likely to achieve recoveries for creditors.

Key element 5: Workload of an insolvency practitioner

A liquidator’s work on an individual company can quickly become unmanageable without sufficient time and resources. When appointments are large or complex—such as those involving extensive litigation—priority is often given to the biggest, most urgent matters. As a result, valid claims, including insolvent trading actions, can remain uninvestigated or never be commenced.

Timely assessment and action are critical for insolvent trading claims: delays can reduce recovery prospects, allow evidence to dissipate, and limit available remedies. Ensuring adequate resourcing and early case triage helps preserve claims, protect creditors’ interests and maximise recoveries. When workload prevents prompt pursuit of a claim, liquidators should document the decision-making and consider referral options to specialist litigators or practitioners.

Key element 6: Evidence of safe harbour protection

Safe harbour is a statutory carve-out to claims for insolvent trading. It protects directors from personal liability for debts incurred while they pursue a genuine and properly documented turnaround plan that is reasonably likely to produce a better outcome for the company than immediate liquidation. To rely on safe harbour, directors should: maintain contemporaneous evidence of the plan and the reasons it is likely to improve creditor returns; show the steps they took to implement the plan; and record professional advice and decisions made during the rescue process. Proper documentation and demonstrable actions are essential, because a future liquidator will examine whether the director’s course of action met the statutory safe harbour requirements before accepting the carve-out.

Case study: Inner West Demolition (NSW) Pty Ltd v Silk [2018] NSWDC 136 (30 May 2018)

This case study illustrates a creditor-led insolvent trading action in which the creditor successfully pursued the director personally. The court entered judgment against the director for insolvent trading and awarded the creditor legal costs in addition to the judgment amount.

Key takeaways: creditors can initiate insolvent trading proceedings, successful claims may result in personal liability for directors, and litigation costs can be recovered on top of any damages awarded.

There is no information in the case explaining why the creditor, rather than the liquidator, pursued the sole director (Mr Silk) in the insolvent trading action. Under Australian law the liquidator ordinarily has the first right to commence insolvent trading proceedings, but a creditor may bring the claim under section 588R of the Corporations Act where the liquidator consents (s588S) or where the statutory period for the liquidator to commence proceedings has expired (s588T). In practice, creditors may act when a liquidator declines to proceed, delays beyond the prescribed timeframe, or expressly grants consent, enabling the creditor to preserve remedies against directors for insolvent trading.

Background

- Plaintiff was Inner West Demolition (NSW) Pty Ltd

- Defendant was Mr Silk, the director of One Build Pty Ltd

- Plaintiff contracted with One Build Pty Ltd to provide demolition services on a building project for a fixed price of $345,000 on 30 August 2013

- Demolition services were provided and a debt incurred by One Build Pty Ltd between September and November of 2013, therefore, the debt was incurred in full before the company was placed in liquidation.

- One Build Pty Ltd (In Liquidation) was placed in voluntary administration on 26 November 2013 and in liquidation on 13 December 2013

- The claim for insolvent trading against Mr Silk was commenced in the NSW District Court on 9 June 2017 by the creditor (Inner West Demolition (NSW) Pty Ltd)

- To succeed in the claim the Plaintiff was required to prove that the company in liquidation traded whilst insolvent and that the director (Mr Silk) knew or had reasonable grounds to suspect that the company was insolvent (and therefore has no defence)

Key facts in the case the court decided against the director

- Both parties relied on expert evidence to establish (or challenge) whether the company was insolvent on the contract date (30 August 2013). The defendant director, however, failed to prove the company was solvent based upon each relevant indicator of insolvency, a key issue in insolvent trading claims — see each indicator of insolvency.

- At the date of liquidation the company had $3.1 million in unpresented cheques, a significant factor the Court considered when assessing the company’s solvency and potential insolvent trading.

- Although Mr Silk engaged an in‑house accountant and gave evidence that he relied on that accountant, the Court held that such reliance was insufficient to absolve the director of liability for insolvent trading.

Decision summary

- For a creditor to make an insolvent trading claim they are required to comply with section 588M of the Corporations Act and this may include obtaining the consent of the liquidator – the Court found that this was complied with

- Taking into account all the expert evidence and materials the Court found that the company was insolvent from 30 June 2013

- The director had not proven any defence because he did not show he had reasonable grounds to expect that the company was solvent

- Verdict for the Plaintiff for compensation for insolvent trading in the amount of $327,332

Case Study: Kleenmaid

Kleenmaid: Case Study in Insolvent Trading and Director Liability

Kleenmaid, an Australian domestic appliance brand, provides a clear and cautionary example of the risks and legal consequences of insolvent trading by company directors. The company’s collapse highlights how prolonged financial distress, combined with dishonest conduct, can result in both civil and criminal liability.

Background and timeline

2008–April 2009: Rumours of financial difficulty surfaced in 2008. In April 2009 Kleenmaid entered voluntary administration, reporting almost $70 million in debts and immediately terminating 150 employees.

May 2009: Administrators reported suspicions that the company had been trading while insolvent since June 2007.

Post-administration: Liquidation revealed the company’s total corporate debt exceeded $100 million, significantly higher than initial estimates.

Legal outcomes

The Kleenmaid liquidations led to criminal prosecutions of former directors for offences tied to insolvent trading and fraud:

- 2015: Former director Mr Armstrong was sentenced to seven years’ imprisonment for fraud and trading while insolvent.

- 2016: Former director Mr Young received a nine-year prison sentence for fraud by dishonesty and criminal insolvent trading.

In both prosecutions, dishonesty was the decisive element that elevated the conduct from potentially civil breaches to criminal offences.

Key legal and practical lessons

- Obligation to prevent insolvent trading: Directors must monitor solvency closely and cease trading if the company is insolvent or likely to become insolvent.

- Evidence and timing matter: Administrators in this case identified a specific period (from June 2007) during which insolvent trading allegedly occurred, demonstrating how retrospective financial review can inform liability.

- Dishonesty multiplies consequences: Dishonest conduct by directors can transform breaches of duty into criminal offences, attracting significant custodial sentences.

- Personal consequences for directors: Beyond company losses and employee impacts, directors face criminal prosecution, imprisonment, and long-term reputational and financial damage.

Practical recommendations for directors

- Implement robust financial monitoring and early-warning systems to detect cash-flow or solvency issues.

- Obtain timely professional advice (accountants, insolvency practitioners, and lawyers) when solvency is in doubt.

- Document decisions and the rationale for continuing or ceasing trading to demonstrate reasoned judgment and good faith.

- Prioritise creditor interests when insolvency is likely, and avoid actions that could be construed as dishonest or designed to conceal the company’s true financial position.

Conclusion: The Kleenmaid case underscores that prolonged insolvent trading, especially when coupled with dishonest conduct, can lead to severe legal and personal consequences for directors. Vigilant financial oversight, transparent conduct and prompt professional advice are essential to reduce the risk of personal liability for insolvent trading.

Case Study: Re Swan Services Pty Ltd (in liq)

Swan Services Pty Ltd operated a large cleaning business in Australia. Liquidators brought an insolvent trading claim against the director (and his wife as a de facto director). The claim was ultimately upheld against the director alone. The judgment of this case illustrated that a Court will not simply determine the quantum for an insolvent trading claim based on the amount of unsecured debt incurred while insolvent. The important decision outlined three key things the Court will look at in determining an amount for an insolvent trading claim:

- A secured creditor whose debts become unsecured by operation of the PPSA upon the commencement of the winding up may be considered unsecured for the purposes of an insolvent trading action;

- Credits to a running account ought to be taken into account when determining the loss or damage sustained with respect to debts incurred during a period of insolvent trading;

- The estimated distributions to creditors in the winding up should be factored in when determining the loss or damage sustained with respect to debts incurred.

Case Study: Not-for-profit (Mansfield v Townend)

In this case, a liquidator brought a claim against a director to recover unsecured company debts totalling around $190,000. The liquidator was unsuccessful, despite being able to prove a breach of all the elements in s 588G(1) of the Corporations Act.

Ms Townend was a social director (voluntary unpaid) of Camperdown Bowling and Recreation Club and had limited education and understanding of her responsibilities. There was no evidence she was aware of the club’s solvency issues in her time there from 2008 up until 2012 when the business was liquidated.

Despite Ms Townend’s lack of understanding of her role and other evidence to suggest she had little to do with the finances, she was still found to be a de jure director.

Importantly, the limited information about the company’s debts that Ms Townend was privy to was held to be inadequate to create a level of suspicion required for the purposes of s 588G(2)(a). It was affirmed that the requisite suspicion must be more than a mere inkling. Adopting a blended objective/subjective test for s 588G(2)(b) Ms Townend was found not to be involved in financial decisions and it was held that a reasonable person in her position would not be aware of any reasonable grounds for suspecting insolvency.

Ultimately, while unsecured creditors suffered loss due to the Club’s insolvent trading, Ms Townend was not held liable because the liquidator failed to discharge the onus of establishing that she contravened s 588G(2) in relation to incurring company debts. The liquidator was also held liable for Ms Townend’s costs.

The judgment noted that the entire situation in relation to Ms Townend and her position was “unusual and extremely unfortunate”.

The key takeaway should be that directorship is likely to be recognised more often than not, even if the director did not carry out many directorial functions, receive pay, or have an awareness of their responsibilities. Moreover, where a reasonable director’s suspicion of insolvency would be aroused, directors should make active inquiries to ascertain the truth.

This case also demonstrates why insolvent trading claims are rare – liquidators risk their money and their reputation in pursuing them.

Case Study: Sparreboom ASIC Disqualification

Mr Sparreboom ran Hedgehog Group Holdings, Sparrk Logistics and Hedgehog Logistics Solutions in road-freight and warehousing. When these companies folded in March of 2022 unsecured trade creditors were owed almost $10 millon and 128 staff were owed A$1.2 million in wages and super. EarlyPay, a debtor-finance provider, also suffered a multi-million-dollar loss after default.

ASIC alleged a range of wrongdoing including the director deleting MYOB records days before liquidation, fabricating invoices, failing to lodge BAS for 11 quarters and preferential payments to related entities (family trusts).

The director received the maximum five-year director ban from ASIC (to 11 Aug 2029) — the harshest available administrative sanction. Interestingly, the liquidators obtained Assetless Administration Fund (AAF) grants to prepare the supplementary reports for this action.

This shows that there is a role for public funding in pursuing insolvent trading matters, where private recovery prospects are low. The investigations which were carried out for the purposes of ASIC considering director disqualification can then be used for further legal action like an unfair preferences case.

What is the likelihood of an insolvent trading claim being brought against you?

So far, so scary. As the director of a SME, what you probably want to know is what the likelihood is of such a claim being pursued against you. The good news is that it’s relatively low.

A claim for insolvent trading is not usually one of the first matters that a liquidator turns their mind to. Their key focus in recovering value is on collecting debts. It is usually at the end of the liquidation process where the possibility of an insolvent trading claim might be considered.

There are no firm statistics on this, but in our estimation, only a handful of insolvent trading claims have been successfully pursued against SME directors in the last fifty years. It is worth noting, however:

- It is not only liquidators who can bring such a claim. It is possible for a creditor to bring a claim for insolvent trading where a liquidator chooses not to. The likelihood of this may depend on how well-heeled your creditors are.

- The Australian Securities & Investments Commission (‘ASIC’) does have the ability to fund a claim where a liquidator refuses, or to assist the liquidator through the AAF. It is unlikely to use this power though, except in the cases of the most egregious director behaviour, though cases like the Sparreboom disqualification suggest that ASIC may be more willing to do so than in the past.

Note also that a liquidator has six years from the beginning of the liquidation to commence an action for insolvent trading. It is not sufficient for the liquidator to have issued a letter of demand within the six-year period; proceedings must have been commenced. This means that even if a liquidation has been finalised, there is still a significant period of time in which the liquidator may decide to commence a claim.

Defences to insolvent trading

There are several defences available to directors against an insolvent trading claim.

- At the time the debt was incurred, the director had reasonable grounds to expect (and expected) that the company was solvent and would remain solvent even if it incurred that debt; note that this ‘expectation’ must be deemed to be reasonable on the facts

- The director expected that the company was solvent at the time the debt was incurred, and that expectation came as a result of relying on information provided by a competent and reliable person who was responsible for providing information as to the solvency of the company

- Because of illness or a similar ‘good reason’ the director did not take part in the management of the company at that time (complete ignorance or the fact that a director was a non-executive director will not satisfy this)

- The director took all reasonable steps to prevent the company from incurring the debt. This can include appointing a voluntary administrator at the appropriate time

- The debt was incurred on or after 19 September 2017 and the safe harbour can be claimed (see below)

What is the effect of the safe harbour?

A liquidator cannot pursue a claim for insolvent trading if the director’s activity is under the protection of a ‘safe harbour’. Section 588G(2) of the Corporations Act 2001 provides that a director is not liable for allowing insolvent trading while they are developing a course of action reasonably likely to result in a better outcome for the company, and incur debts in the process.

Liquidators are risk averse – they want strong evidence to support a claim before they will run it in court. At the end of the day, they are accountants on an hourly rate so they are not incentivized to be agressive. If there is a real prospect that your behaviour was protected by a safe harbour, they are unlikely to risk bringing an insolvent trading claim in court.

What is the effect of Small Business Restructuring?

Small Business Restructuring (Restructuring under Part 5.3B of the Corporations Act 2001) is a relatively new external administration procedure, introduced in 2021 especially for SMEs. It is only available for businesses that have no more than $1 million in debt and are otherwise up-to-date with their tax lodgments and payment of employee entitlements.

Such businesses can appoint a specialist insolvency practitioner — a restructuring practitioner (RP) — to prepare a restructuring plan for the business. If agreed to by a majority of creditors in value, the debt is restructured and the business can continue trading

Crucially, unlike Voluntary Administration, during the restructuring process, the directors remain ‘debtor in possession’ and are able to continue trading while the process is ongoing. This means appointing an RP can be a useful mechanism for eligible directors to avoid a claim for insolvent trading whilst continuing to have day-to-day control of the business whilst the process runs.

How long does it take to run an insolvent trading claim?

If a liquidator decides to bring an insolvent trading claim, it helps to understand the typical stages and approximate timing. Exact timeframes vary, but the usual process follows these steps:

- Liquidator appointment and initial investigation: Appointment triggers a comprehensive investigation of the company’s assets and affairs. The liquidator must provide a statutory report within three months, but investigations commonly continue beyond that.

- Asset recovery (can begin immediately): The liquidator will recover realisable assets, typically by selling plant and equipment and collecting outstanding debts.

- Review for other recovery actions (up to about 2 years): The liquidator assesses whether to pursue claw-back remedies such as unfair preference claims or transactions at an undervalue. These enquiries and any related litigation or negotiations can take up to two years or longer depending on complexity.

- Examination and evidence-gathering: Before suing for insolvent trading, the liquidator often conducts examination proceedings and issues process to obtain books, records and witness evidence from company officers and advisers to form a clear case.

- Letter of demand and negotiation (often 1–2 years after liquidation starts): If the liquidator decides to pursue a director for insolvent trading, they typically issue a letter of demand setting out the claim and inviting settlement within a limited period. If negotiations fail, the liquidator may commence court proceedings.

How to prepare for an insolvent trading claim

Just as when dealing with the police, you have the right to remain silent, but only initially. While there are statutory obligations to provide a range of materials to liquidators, as a director you need to be careful not to say anything else that incriminates you. For example, if you have not been keeping adequate financial records and you admit this to the liquidator, this admission could be used as part of the case against you.

Once you are being interviewed, with the prospect of a criminal prosecution, the best advice, as stated above, is to exercise your right to remain silent. As this can be difficult in a liquidator’s examination, you should seek legal advice before this occurs. Important things to consider include:

- As soon as the letter of demand is received, talk to a lawyer. That lawyer would be likely to advise you to be careful not to make any ‘admissions’ at an early stage;

- In order to collect documentary evidence and oral admissions, you should engage your lawyer to appear in court and assess the weight of the evidence and asset position that you are in (you might consider an out of court settlement);

- A common flaw of directors is pursuing the ostrich strategy – sticking their head in the sand until it is too late. It is important to seek legal advice early and try to make sensible decisions without overreacting.

What should you think about when briefing a lawyer?

The possibility of an insolvent trading claim on the horizon is a key reason why you may need to seek legal advice prior to, or in the process of liquidation. Lawyers are the only ones that fully understand litigation and the risks you face. In addition, your discussions with a lawyerare protected by legal professional privilege. By contrast, your discussions about possible insolvent trading claims with an accountant are not and if discovered, could be used against you in future proceedings. You should ask for an initial discussion with a lawyer to begin assessing your risk, and make sure you only seek out experienced insolvency lawyers who can develop a tailored strategy with the best prospects of success.

Key Takeaways

- Creditors can bring insolvent trading claims, but in practice liquidators usually commence them.

- Creditor-initiated actions are uncommon because they require substantial funding and the ability to prove the company was insolvent and overcome any director defences.

- Regulatory involvement (e.g. ASIC) or liquidator action is not guaranteed—underfunding and resource limits often explain why claims are not pursued by those parties.

- Liquidators are generally reluctant to sue directors of small and medium-sized enterprises for insolvent trading unless there is clear evidence of reckless or dishonest conduct.

- Successful insolvent trading claims can have serious civil and reputational consequences for directors, including personal liability for company debts.

- Practical barriers to bringing claims include evidentiary difficulties, the cost of litigation, and limited recoveries; these deter many liquidators from proceeding.

- If you are the subject of an insolvent trading claim, or concerned about potential exposure, obtain prompt advice from a specialist insolvency lawyer to assess risks and defences.