Zombie Companies Survival Guide: Diagnose, Stabilize, and Revive Your SME

What is a zombie company? Understand zombie companies and their warning signs. These companies struggle and impact the economy.

Table of contents:

- What is a zombie company?

- Where did the term ‘zombie company’ come from?

- Industries prone to zombie companies

- What mistakes do directors make?

- How do zombie companies get tipped over the edge into insolvency?

- How can zombie companies fix their problems?

- What have regulators been doing about zombie companies?

- What is the impact of zombie companies on the wider economy?

- How should directors decide whether to restructure or wind up a zombie company?

- Causes and symptoms of zombification: John Argenti

- There are four main symptoms of zombification/business failure

- The three types of zombie company

- Company survival kit

- Cultural signs of a zombie company

- Case study: Darrell Lea

- Case study: Borders Books and Angus & Robertson

- Australian management problems

- Conclusion

What is a zombie company?

A zombie company is a business that barely scrapes by and is always short of cash. In accounting terms, it covers most of its running costs but is never able to generate a profit margin.

According to BIS Oxford Economics, a zombie company can be defined as an operating business with a ratio of earnings before interest and tax (EBIT) to interest expenses below one. The lower the ratio, the greater the likelihood of the company failing.

The problem with zombie companies is that they can be easily tipped over the edge into insolvency when something goes wrong. Sometimes the boiling-frog analogy is accurate – zombie companies move from one crisis to another without realising their financial position is getting worse – until they are finally boiled (financially). Insolvency is a position in which a company is unable to pay its debts, regardless of whether sales are forecast to increase. The main takeaway is that the difference between a zombie company and an insolvent company is that while a zombie company is sick and might be dying, an insolvent company is terminal or already dead.

When large corporations—often deemed “too big to fail”—slip into becoming a zombie company they frequently receive government or lender bailouts; small-to-medium enterprises (SMEs), defined as businesses with fewer than 200 employees and accounting for 97% of Australian firms per the Productivity Commission, rarely have that safety net and therefore face far greater risk of collapse.

Where did the term ‘zombie company’ come from?

So where did zombies come from? The term ‘zombie company’ to describe a low profit, precarious business was first applied to Japanese firms which sought the support of national banks after the collapse of the Japanese asset price bubble in 1990. One of these firms, which employed almost 100,000 people was described by the then Japanese Finance Minister as being ‘too big to fail’, a phrase now often used when justifying a bailout.

In 2008, companies receiving bailouts as part of the US Troubled Asset Relief Program were referred to as ‘zombies’, ahead of the devastating effects of the Global Financial Crisis – the term has been widely used in the US since.

In 2016, China recognised the issue of ‘zombie enterprises’ and proposed to close and reorganise several key public industrial companies following the stock market crash.

Before 2020, ‘zombie company’ was not a term many Australians were familiar with. However, the introduction of several government and central bank policies designed to support businesses through the financial impact of COVID-19 and lockdowns had many commentators concerned about how many zombie companies are eating up resources and perpetuating debt. JobKeeper, bank payment extensions, looser enforcement of statutory demands and the extension of the safe harbour all allowed zombie companies to keep trading, remaining dependent on high liquidity, negative interest rates and huge fiscal stimulus. ‘Zombie company’ is now a term Australians should endeavour to become familiar with.

Zombie companies are a moral hazard – they encourage and normalise uncommercial companies to continue trading, with negative effects on the economy. SMEs that are zombie companies are also likely to drain the energy and wealth of their owners.

Industries prone to zombie companies

SMEs are by nature brittle due to thin working capital and dependence on their owner’s wealth for support, and as such, they are highly vulnerable to becoming zombies. However, the primary cause of a zombie company is its industry. Zombie companies mainly crop up in mature industries where practices are well established, there are low barriers to entry, business is competitive and margins can be squeezed by customers. Below are some of the key industries plagued by zombie companies:

- Building and construction companies: They are at the mercy of larger builders and their tight cash flow means that if they lose one project they may be pushed into insolvency

- Transport companies: They have high capital and labour expenses (including insurance) and losing one big customer can push them into insolvency

- Retail and hospitality: Currently retail businesses are under enormous pressure from online competitors and the erosion of sales margins through other changes

- Professional services: High labour costs and market competitiveness means professional service providers of all types could become price takers

- Mining services: The mines push risk down on service providers so that they bear the risk of any downturn

What mistakes do directors make?

Directors often make a range of key errors in their responses to weak economic returns. These include:

- Working ‘in’ the business but not ‘on’ the business – what is the root cause of the problem after all? There is an important difference between the ‘symptoms’ of zombification (i.e. low profits) and what the true cause of these symptoms are. Only by addressing the true cause will the directors be able to execute a successful turnaround.

- Using expensive finance facilities such as receivables finance, caveat loans or credit cards to fund working capital shortfalls

- Failing to look properly at their corporate structure and continuing to invest sweat capital in an out-of-date structure

- Hiring the local solicitor and avoiding good quality lawyers who can develop a dependable litigation strategy

- Avoiding their accountant and bookkeeper and failing to make sure their accounting software is fully reconciled

- Putting prestige over profits by not focusing on the 20% of customers that deliver 80% of profit

- Avoiding conflict with employees by not managing by objective – trying to be mates not managers

How do zombie companies get tipped over the edge into insolvency?

Because zombie companies do not have the resources or strategies in place to account for unexpected developments, when these developments occur, they can tip zombie companies over the edge financially.

- Management issues – such as a breakdown in the relationship between the owners. This causes tension in the workplace, diverts the management’s attention away from the business and allows business management to fall by the wayside.

- Loss of important customer – if a customer that brings in most of the revenue (the ‘Whale’) terminates their contract or a key contract is lost to a competitor, this will likely constitute an unmanageable drop in income for a zombie company. Without taking swift and decisive steps to cut costs or recoup the losses (which zombie companies are rarely able to do), the company will likely fail.

- Big project out of control – a key project is either failing or draining cash flows. For a zombie company that does not have a good handle on its financial situation, the big project will likely continue to cost the company more money than it makes, until the business fails.

- Sickness – illness such as depression may hold back the proprietors, diverting their attention away from the business and causing a decline in morale, productivity and accountability which can lead to losses.

- Fraud – key person in the business takes business opportunities or cash away from the company.

- Constraints – a key issue that the business has faced becomes mission critical. Extra constraints are unlikely to be handled well by a business that is out of touch with its finances and people.

These problems would not spell the end for a securely profitable company, but for zombies, they are compounded by a lack of up-to-date financial information, insufficient working capital and creative accounting. This means the scale of problems are rarely properly understood, and businesses are not in a position to work towards addressing them.

How can zombie companies fix their problems?

The typical actions that help directors to get a handle of their situation are:

Analysis of the problem

- Root cause analysis regarding profit margin improvement

- Staff evaluation, termination and new hires

- Improved management accountability and staff role alignment

- Improvement of customer mix targeting

- Dealing with creditors regarding payment terms

- Representing the proprietors in ongoing litigation

- Working with accountants to ascertain their financial position

- Evaluating financing and equity injection options and offers

- Considering whether a restructure is feasible

- Evaluating the risk to the personal assets of directors and proprietors

- Recovering claims owing to the company

- Discussions with stakeholders in the business

- Identification of toxic employees

Execution of a restructure

- Negotiations with creditors and documentation of outcomes

- Termination of toxic employees

- Cashflow planning and rationalisation of expenses

- Termination of unprofitable customers

- Implementation of focus strategy to improve new clients taken on board

- Performance management of employees

- Sale or exit of business

- Working with accountants to finalise accounts and undertake remedying transactions

- Drafting contractual and transactional documentation to improve the structure

- Engagement of an insolvency practitioner (liquidation or voluntary administration)

- Representation at creditor proceedings

What have regulators been doing about zombie companies?

During the Covid-19 pandemic, there were a range of regulatory mechanisms and actions designed to make it easier for companies to survive difficult trading conditions: This included JobKeeper benefits, a new safe harbour from insolvent trading, limitations on statutory demand collections, and a more relaxed approach from ATO to tax collection of distressed businesses. While arguably necessary, these measures also had the effect of exacerbating the problem of zombie companies — companies that should have been wound up were able to continue operating.

Over the last several years, however, regulators have sought to turn this around and have gotten increasingly ‘firm’ with zombie companies and other distressed businesses, including:

- ATO issuing a record number of Director Penalty Notices — 26,702 in 2023-24 for more than $4.4 b in company debts

- Faster implementation of garnishee notices (time between first reminder and enforcement cut to as little as 23 days)

- Forcing earlier ‘GST touchpoints’: From 1 April 2025 about 3,500 chronically non-compliant small businesses were pushed from quarterly to monthly GST lodgement.

According to 2025 ASIC data, corporate insolvencies are now at a level not seen since the Global Financial Crisis, with 3,306 companies going insolvent in the first quarter of the year. In theory, this should mean a significant reduction in the number of zombie companies. The additional good news is that there is also a record number of Small Business Restructuring appointments, indicating efforts to turn around insolvent companies (whether zombie or not).

What is the impact of zombie companies on the wider economy?

According to a 2019 report from KPMG, one in seven companies listed on the ASX trades in zombie territory. Also considering that SMEs are more likely than larger, established companies (i.e. those listed on the ASX) to be zombies; from this, we can infer that a significant percentage of operating Australian businesses are zombies, and zombie companies pose a significant risk to our economy.

According to the Organisation for Economic Cooperation and Development (OECD) zombie companies generally cost the economy by hampering productivity growth, diverting credit, investment and talent away from efficient and sustainable businesses. They also slow the rate at which best practices and new technologies are adopted across an economy. In Australia, zombie companies hold an estimated $5 billion in shareholder capital, which could be more effectively invested elsewhere. At a company level, zombies, which are inherently uncompetitive, negatively impact pricing power, reduce return on equity and have the effect of lowering market valuations of otherwise healthy companies.

How should directors decide whether to restructure or wind up a zombie company?

If a company is a zombie, and directors make no changes to the business and do not enter external administration, it will inevitably fail at some time. So, how far gone is too far gone? In order to determine whether a zombie company can be salvaged through a restructure or whether it would be economically wiser to proceed immediately to winding up, directors should ask themselves a series of questions. The first steps usually employed are on the expense side to cut costs and the income side to employ a more focused strategy.

Zombie company Checklist:

What are the market forces we need to be attuned to?

- e.g. supply/demand, government, speculation/expectation, international forces

- What do the movements in these market forces reveal about the industry?

- How can we tailor our offering to be competitive in this market?

- Can the company meet these forces? At what cost?

2. What are the existing debts?

- What is owed to whom?

- What is the nature of the relationship with the creditor?

- Can a repayment plan or debt forgiveness be negotiated?

What is the estimated return of a wind up vs. a turnaround option?

- Is an informal restructure, such as through the safe harbour from insolvent trading, an option? How long would a restructure take to pay off and can money be sourced to fund it (difficult for SMEs)?

- Is a formal restructuring option desirable? If debts are less than $1 million Small Business Restructuring under Part 5.3B of the Corporations Act 2001 (Cth) is a possibility. If the debt is higher, then Voluntary Administration may also be an option.

- What will be the effect on the goodwill value?

- What kind of advice will be required?

- What returns will a wind up generate?

Directors of zombie companies should seek out pre-insolvency advice from a professional in order to decide what the best course of action is (restructure or wind-up) for their company. Read our article about choosing a pre-insolvency adviser for more information.

A successful restructure should be planned and supervised by an experienced adviser and, after implementation, supported by a turnaround board to monitor progress and hold management accountable. Restructuring options vary by size, complexity and creditor position; the right choice can prevent a distressed or “zombie company” from drifting indefinitely and eroding value. Common approaches include:

- Safe harbour from insolvent trading (informal): Allows directors breathing space to pursue a turnaround without immediate personal liability for insolvent trading, provided they develop and meaningfully pursue a plan. Read our article on the safe harbour here for more detail.

- Small business restructuring process: A formal, creditor-involved process for eligible small businesses to restructure debt and operations with the assistance of a qualified adviser. See our guidance on Small Business Restructuring for further information.

- Voluntary administration: A formal procedure that stays creditor actions while an administrator assesses the company’s prospects and proposes a plan (such as a Deed of Company Arrangement) to maximise return to creditors. Read our articles on voluntary administration for more information.

- Debt rescheduling and renegotiation: Direct negotiations with lenders to extend terms, reduce interest, or provide temporary relief; often the fastest way to stabilise liquidity and avoid formal insolvency processes.

- Recapitalisation and equity conversion: Bringing in new capital or converting debt into equity to strengthen the balance sheet—may involve existing shareholders, new investors, or creditor-equity swaps.

- Operational turnaround: Immediate cost reductions, asset rationalisation, management changes, and focused sales or divestments to restore cash flow and profitability.

- Sale, merger or structured exit: Selling the business or key assets (including through a controlled sale during administration) or pursuing a merger to preserve value and jobs where standalone recovery is unlikely.

Choosing the right mix of these options depends on creditor positions, cash-flow forecasts, stakeholder objectives and whether the business can return to viable trading. Early adviser involvement and active governance (for example via a turnaround board) are critical to prevent a zombie company outcome and to give any restructure the best chance of long-term success.

Causes and symptoms of zombification: John Argenti

In his famous book Corporate Collapse, John Argenti identifies eight main causes of zombification/business failure. This is an excellent model to help company directors guide their root cause analysis before starting the turnaround process. The causes of corporate insolvency are set out below:

Management problems

Effective management is key to the success of a business. Without someone overseeing the business function as a whole, it can be very difficult to spot big picture problems which can lead to zombification or insolvency. According to Argenti, there are six main issues that can occur with management.

- One-man rule: the chief executive dominates colleagues instead of leading them, reducing morale and limiting effectiveness and collaboration.

- Non-participating board: poor engagement by the board in company matters leads to things being missed.

- Unbalanced top team: senior staff do not have a spectrum of skills or a diverse educational background which means they have gaps in knowledge about industry, business or people which lead to failures.

- Lack of management depth: broadly, a lack of management training/skills which leads to poor management.

- Weak finance function: lack of utilisation of finance experts which means that finances are not managed and planned accordingly, leading to a lack of ability to adapt to business challenges and a lack of awareness of the financial position.

- Combined chairman/chief executive: combining roles creates a lack of accountability at the top of the management hierarchy due to too few people being involved.

Accountancy information is poor

Accurate accountancy information is vital for a business to understand its own position. Without it, directors will not be able to tell whether or not they are making a meaningful profit. The four most crucial types of accountancy information are:

- Budgetary control: effective use of budgets to plan the business’ path forward (i.e. growth, saving, new initiatives/products, etc).

- Cash flow forecasts: early detection of potential shortages so that changes to spending can be made if losses are predicted.

- Costing systems: effect of product cost on profit should be known and managed so that pricing is accurate.

- Valuation of assets: accurately determine the financial position and how much money could be recouped from a liquidation or sale of select assets.

Insufficient responses to external change

A continuously changing business environment is guaranteed. A weak business will not be well equipped to respond to change, thereby indicating that they may be a zombie company. There are five main types of change that a company should be able to adapt to:

- Competitive trends: developments in products or competitors (i.e. announcement of new products or mergers of competitors)

- Political change: a shift in governmental and/or international attitudes towards business (if this is negative, it can impact resources, markets and financing)

- Economic change: macro-economic factors such as foreign exchange rates, inflation, interest rates and the economic cycle can affect profits

- Societal change: changes in lifestyle or beliefs (i.e. climate change/consumer protection) can shape consumer behaviour

- Technological change: developments in technology within the industry could increase competition, research and development costs and change the nature of the business

Failure to understand constraints

Businesses rely upon scarce resources, regulations and societal demands that need to be carefully managed. A constraint is a natural limit of some kind that a business faces. Generally, these are imposed by external parties on the way the company trades and relates for some form of accountability for its actions. Even the smallest company may not be able to withstand adverse attention in social media.

Overtrading

Overtrading occurs when a company boosts sales at the expense of profit margins in a short-sighted push for growth. That strategy often forces heavier borrowing to fund operations, creating a widening financial gap; in smaller firms this can quickly lead to mounting tax and creditor debts. Left unchecked, persistent overtrading can turn a viable business into a zombie company—one that survives on frequent refinancing and minimal profitability but lacks the resources to invest or recover.

The big project

An undertaking that is large compared to the resources of the company. The project fails because costs and times are underestimated or revenues overestimated. If the project is not cash flow positive, although it promises growth in the future, it can be too much to bear in the immediate future.

Too much gearing

Gearing rises when a company increases its reliance on borrowed money. While some debt can finance growth, excessive leverage—what pushes a business past its industry-specific safe limit—can turn a firm into a zombie company, able only to service interest payments rather than repay principal or invest in operations. Such high-geared firms are especially vulnerable to economic downturns: reduced revenue or higher interest rates can leave them unable to cover obligations without cutting investment, shedding staff, or seeking rescue financing.

- Key indicators: rising debt-to-equity or debt-to-EBITDA ratios, interest coverage close to or below 1, persistent reliance on refinancing.

- Typical consequences: constrained capital expenditure, weakened competitive position, higher default risk, and potential prolonged survival as a zombie company that drags on productivity.

- Management response: deleveraging through asset sales, recapitalization, cost restructuring, or negotiating more sustainable debt terms to avoid becoming a zombie company.

Normal business hazards occuring (in conjunction with one of the above)

Every business faces risk in some form or another that needs to be managed. Events which clearly cause the failure of companies but being normal, foreseeable hazards of any business, should not have had the capacity to cause failure. These events cause failure because the company is already weak (i.e. a zombie), and may include a fire on the premises or movements in market share.

There are four main symptoms of zombification/business failure

In Corporate Collapse, John Argenti identifies four key symptoms of zombification—signs that a company is becoming a zombie company—that directors should evaluate during their analysis phase; these symptoms are separate from the causal factors Argenti discusses elsewhere.

Financial ratios

Financial ratios can be useful to identify symptoms of failure, but while they might show something is wrong, they do not provide enough evidence to predict collapse. Inflation can seriously erode their effectiveness and they are also vulnerable to ‘creative accounting’ and thus not entirely reliable. Financial ratios include:

- Altman’s Z score

- Working Capital/Total Assets

- Retained Earnings/Total Assets

- Earnings Before Interest and Tax/Total Assets

- Sales/Total Assets

- Market Value of Equity/Book Value of Total Debt

- Current ratio or current assets/current liabilities

- Quick ratio or cash plus debtors/current liabilities

- Profit/sales or ‘margin’

- Sales/fixed assets

- Cash flow/debt

- Stock + debtors – creditors/long term capital

- Long term loans + equity capital/fixed assets

- Price/earnings

- Other industry specialised ratios

Once the above ratios have been calculated the director should compare them to industry averages to measure the level of deterioration faced by their company.

Creative accounting

Managers could choose to use creative accounting tactics to hide the extent of the company’s problems, which reduces the effectiveness of financial ratios (above). Creative accounting techniques (which could amount to accounting fraud, which is illegal) can include:

- Delay in publishing results

- Capitalising research costs

- Continue paying dividends (even if equity or loans are needed to do so)

- Cut expenditure on routine maintenance until a major renovation is needed which can be treated as capital

- Treat extraordinary income as ordinary income

- Bring more results from subsidiaries into consolidated accounts progressively

- Retaining company assets under names of personal proprietors

- Inaccurate asset valuation

- Capitalising training costs, interest charges on loans, IT costs and advance payments

- Use inflation as a smokescreen to revalue assets

- Value stocks of finished products at market selling price instead of cost

- Hold back output before inspection

- Invent customers and transport

- Set a sales target; if sales fall short, take the percentage short out of this years’ accounts and defer to the next year

- Fail to revalue assets so that depreciation looks adequate compared to book value even though it is too low

If management resorts to these creative accounting techniques, they are likely trying to placate creditors—such as the ATO or a lender—and defer current problems, effectively prolonging the life of a zombie company instead of addressing underlying financial weaknesses.

Non-financial symptoms

There are many non-financial symptoms exhibited by failing companies, although companies that are not failing may also display them. These will be very different for each industry and even each company. However, examples include low morale, decline in service or quality, and marking down of the company share price.

The last few months

Terminal stage — the point at which a zombie company is on the brink of collapse: multiple financial and operational symptoms intensify (chronic negative cash flow, escalating debt service covered only by new borrowing, collapsing revenues, employee departures, supplier refusals to extend credit, and loss of customer confidence). At this stage restructuring options are severely limited: stakeholders have little appetite or capacity to inject fresh capital, lenders demand repayment or enforce collateral, and any turnaround plan faces prohibitively high costs and low probability of success. In practice, recognition of this terminal phase signals that salvage efforts will likely fail and voluntary administration may need to be commenced.

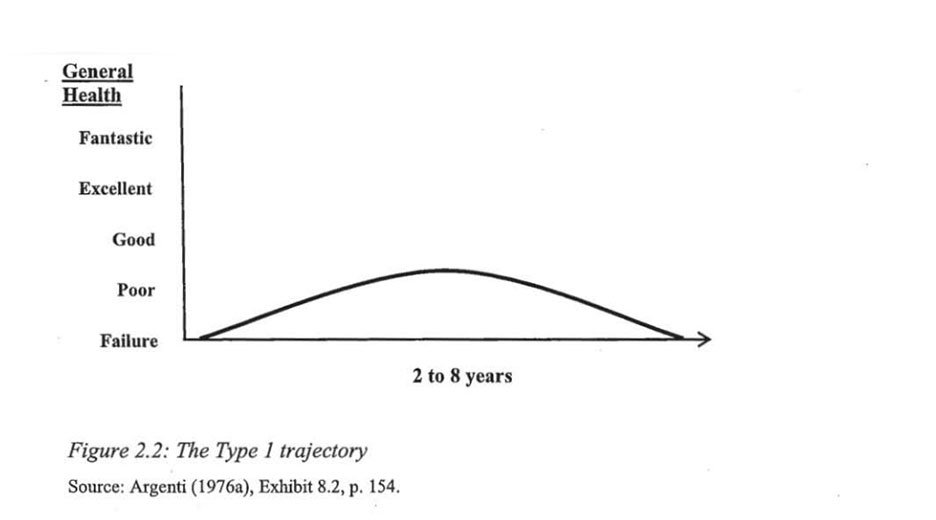

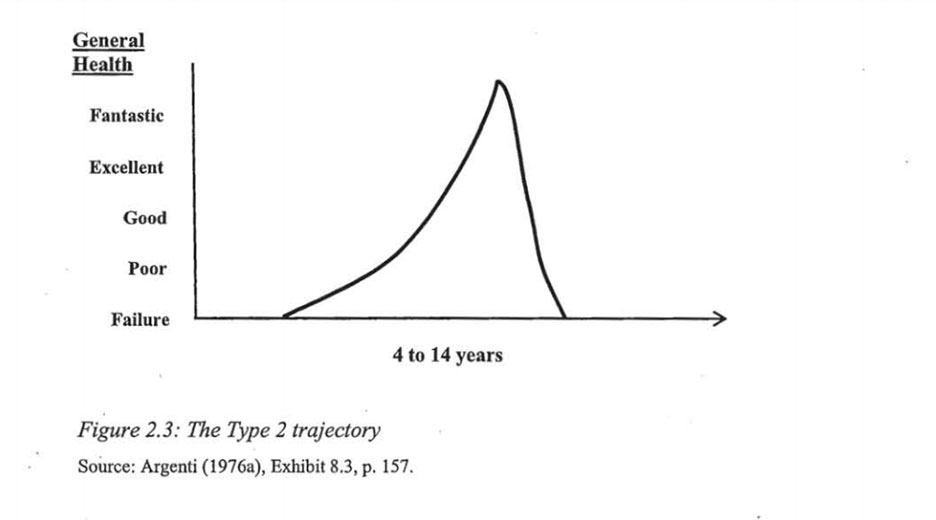

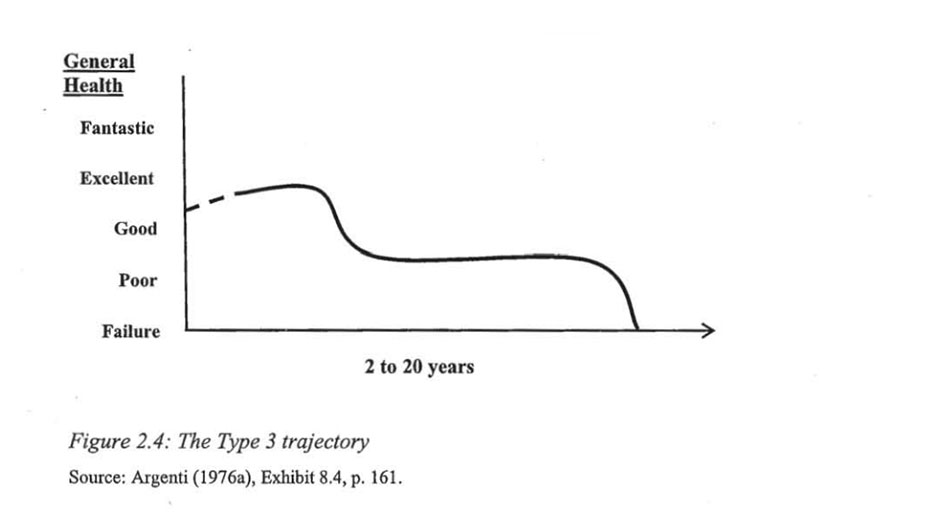

The three types of zombie company

According to Argenti in ‘Corporate Collapse: Causes and Symptoms’, there are three distinct types of failed company. We have named and explained them below:

Type 1: The Submarine

This type only applies to new companies. This type of company charts a continuously low path before ‘sinking’ – i.e. it was a zombie company right from the start and never made a meaningful profit. The problems with the company were there from the beginning, and there was likely nothing of value to save in terms of goodwill. This is a less common type of zombie company given its age, but it clearly fits the description.

Type 2: The Space Shuttle

This type applies to young companies. A type 2 company looks similar to a type 1, but for example the proprietor may have an entrepreneurial personality. The business trajectory is different: it launches successfully before rapidly declining. These companies are rare and are typically characterised by unsustainable growth. They cannot really be characterised as a zombie company because they lack the extended ‘plodding along’ period: instead, they fail fast and dramatically.

Type 3: The Kite

These types of failures occur in companies that have been trading for many years. However, this type of business will remain operational for a long period once entering the zombie phase. Type 3 is the classic zombie company, charting the complex path of ‘good performance’ followed by losses, a plateau and an ultimate failure.

Company survival kit

To fix a zombie company (i.e. restructure it) you must first address the symptoms (damage control) and then address the causes (long term fix). In the first stage of damage control, it is easier to reduce expenses than quickly build up income through a loan (which a struggling company is unlikely to be approved for) so directors should start here. It is important for directors to manage by objectives (identifying and focusing on key objectives) in order to keep on track. Ultimately, businesses need to change their competitive position. This is a slow-moving ship; it is better to not try and change strategy completely, but make small, manageable, incremental changes to take advantages of the existing customer base and goodwill the company has.

Cultural signs of a zombie company

There are several cultural signs that may indicate a company is a zombie. These include:

Complacency

- Arrogance

- Condescension (within business and to competitors)

- No desire to learn about new technology or new strategies

Unwavering pursuit of a dated vision

- Reluctance to innovate in the name of loyalty, i.e. “we know what the customers want better than they do”

Shunning criticism (internal and external)

Reliance on debt rather than growth through retained earnings

Lack of investment

-

- In research and development

- In progress

- In people

Case study: Darrell Lea

Beloved Australian chocolatier Darrell Lea is over 95 years old in 2025 and remains a trusted and iconic brand. But in 2012, all of that was at risk when the company collapsed. It entered voluntary administration and Darrell Lea’s 700 staff faced huge uncertainty, with half of the brand’s store fronts closing and hundreds ultimately losing their jobs.

The company was purchased for around $25 million by Queensland’s Quinn family, serial entrepreneurs who executed a significant restructure, transforming this company from a zombie into a reborn success – in 2018 the company was sold again to the tune of $200 million. The Quinns did not purchase the remaining store fronts, resulting in 27 further closures and over 400 redundancies. Ultimately, staff numbers were reduced from over 700 to around 200.

Darrell Lea was a Type 3 zombie company for many years before its collapse. It had excellent brand recognition, but failed to adapt to changing consumer behaviour. Darrell Lea was poorly managed before 2012 – not high end enough to make their store front experience and presence profitable (like competitor Haigh’s Chocolates) but also failing to take advantage of the tendency of shoppers to impulse buy their chocolate by positioning themselves in retailers like supermarkets or petrol stations. Their products remained largely unchanged and unsuited to the way purchasers purchase high quality chocolate. The cost of maintaining staff and shop fronts, a poor marketing strategy which did not take adequate advantage of their brand equity and the failure to develop new products is what likely caused the failure of the business.

The Quinn family, in realising the untapped potential of this Aussie favourite, executed an extremely successful turnaround, quadrupling the company’s value in just six years. By consolidating the company headcount, abandoning shop fronts and doing distribution deals with IGA, David Jones, Big W, Australia Post and independent distributors (most notably pharmacies), Darrell Lea was able to improve the availability of their product to older Australians familiar with the brand who frequent independent grocers, post offices and pharmacies. This is likely what led to the successful turnaround.

Since the 2018 sale, Darrell Lea has only soared higher. The introduction of its chocolate block range in 2019, featuring beloved flavours including Rocklea Road, Liquorice, Fruitier and Nuttier, Caramel Craving and Peanut Brittle has been hugely successful, positioning the product as a major domestic competitor to Cadbury’s Marvellous Creations.

The Darrell Lea story is an excellent example of how zombie companies can be effectively restructured with the right market insight and turnaround plan.

Case study: Borders Books and Angus & Robertson

REDGroup Retail, owner of Borders Booksellers and Angus & Robertson, once accounted for 20% of Australia’s book market. Another classic example of a type 3 zombie, the parent company of both booksellers entered voluntary administration in 2011, and the brands were never revived. So what went wrong?

The failure was blamed on the online book market (i.e. Amazon, Booktopia, the Book Depository), a strong Australian dollar, import restrictions, high rental prices for store fronts and overpriced products.

However, all of these problems could have been addressed by good management, which these booksellers did not have. Strategic marketing failures and an unwillingness to adapt from traditional bookseller to online retailer (informed in part by a lack of knowledge about changing consumer behaviour and the move towards the e-book market) is what ultimately closed the book for this business.

REDGroup made losses for three consecutive years (FY2008, FY2009, FY2010) before its collapse – a clear sign that management refused to recognise and address the signs of zombification before it was too late. Importantly, this poor performance was already occurring before the Australian dollar began to strengthen and before e-books began to take off.

Between 2008 and 2011 the bookselling industry underwent dramatic change, and well-managed retailers adapted quickly. Chains such as Borders and Angus & Robertson failed to offer online catalogs or embrace e-books, leaving their physical stores less relevant. Because these retailers targeted a broad, unspecialised customer base, the in-store experience added little differentiated value, turning once-viable businesses into de facto zombie companies that struggled to generate growth. For example, in 2010 REDGroup’s online sales represented only 4% of total revenue, highlighting the cost of neglecting digital channels.

REDGroup did not invest in marketing, management, staffing or products that would assist them in transitioning their expertise in traditional retailing to the changing market. By sticking their heads in the sand and continuing on with what they knew (i.e. adopting a ‘we know what the customers want better than they do’ approach) they carved their own tombstone. Even the older demographic, generally reluctant to accept change, were faster to adapt to the new way of reading books than Borders and Angus & Robertson were, accelerating the entire process.

However, REDGroup did at least try to enter the e-book market by working with Indigo (Canada) to sell the Kobo e-reader. However, this product was far less attractive to consumers than the Kindle and iPad, and ultimately did not sell well – something that could have been predicted with a better understanding of the online market.

REDGroup missed a major chance to become the “Amazon of Australia” by failing to read market signals and adapt; as a result, this zombie company collapsed under the weight of strategic complacency, poor execution, and resistance to necessary change.

Australian management problems

Much of the way a business is run can be traced back to culture, which itself is informed by the attitudes and beliefs of those that run the business. There are several key management problems that are unique to Australia, and especially Australian SMEs. These include:

People try to be mates, not managers

The Australian notion of mateship and larrikinism might make friends, but it won’t make good workers. Managers who seek to be friends with their staff are likely to find difficulty commanding respect and curating authority. While civility, kindness and understanding from managers is very important in creating a good workplace culture, it should not be at the expense of professionalism and clearly defining the relationship.

Barbecue approach to management

Australians love a barbecue. They taste great, and they’re easy – all you have to do is stand there in your thongs with a beer in one hand and tongs in the other, occasionally flipping the sausages while having a side conversation with a mate and plenty of freedom to watch your kids playing. While this laid-back, casual approach works just fine for cooking a Sunday night meal, it doesn’t work for managing a business. If managers are focusing on something else, and only glancing over at the business every now and then to make minor changes, huge problems can be missed and you won’t realise something is burning before it’s too late.

Australian exit rates

While many struggling businesses do not become insolvent, this doesn’t mean they don’t end – and many zombie companies wrap up this way (i.e. exit or cessation as opposed to formal insolvency). This is the case for many different reasons – the Productivity Commission’s 2015 Report on Business Set up, Transfer and Closure goes into them in depth, but some will be summarised here.

- Lack of innovation: only a small proportion of Australian businesses are truly innovative. According to ABS statistics, it is estimated that less than 2% of businesses (new and existing) introduced a product that was ‘new’ to the World or Australia. Innovations in operational processes or marketing strategies were even less common, while the protection of intellectual property rights through patent applications was only sought by 0.1% of businesses, below the reported global rate.

- Business exit: the vast majority are voluntary, and 90% are not due to formal insolvency. Businesses exit for a range of reasons, including family succession, sale of business, merger, transfer to employees, management buyout, initial public offering, private placement and cessation. Small businesses account for over 99% of all set-ups and closures. Entry and exit rates are higher for small businesses and unsurprisingly, new businesses have a lower chance of survival than already established businesses.

- External conditions: The set-up, transfer and closure of businesses are either fostered or hindered by the existence and interaction of a number of factors (i.e. structural, regulatory, cultural and financial) that together make up a business ecosystem. When these factors do not align, business exit is common.

Conclusion

Zombie companies may appear harmless while they limp along, but when they are artificially propped up they pose a significant risk to the broader economy, creditors and employees. This article explained the common causes of zombie companies, how to identify them and the specific risks they create. As regulators increase scrutiny, the term “zombie company” will become more familiar in Australia and beyond, and SME directors face a difficult road that can bring stress, financial loss and wasted resources if the business continues to drift.

For directors determined to turn a zombie company around, decisive, timely action is essential. Below are practical takeaways and steps directors can implement to improve the company’s prospects and reduce personal and stakeholder risk:

- Diagnose the problem quickly: Conduct an honest, data-driven assessment of cash flow, profitability, and viability of core operations. Identify which parts of the business are profitable and which are loss-making.

- Prioritise cash management: Preserve liquidity by cutting non-essential spending, delaying non-critical capital projects, tightening working capital, and accelerating receivables collection.

- Rework debt and obligations: Open negotiations with creditors, lenders and landlords to restructure debt, extend maturities, secure covenant waivers or obtain temporary relief. Explore refinancing only if it improves sustainability.

- Reduce costs and simplify operations: Target rapid, high-impact cost reductions, rationalise product lines, exit underperforming segments and streamline processes to restore margin quickly.

- Focus on core strengths and customers: Reorient resources to the business’s most competitive offerings and key customer relationships to stabilise revenue.

- Consider strategic options: Evaluate asset sales, joint ventures, mergers, or a controlled wind-down of non-core units. If turnaround is not feasible, plan an orderly insolvency process to minimise losses.

- Engage professional advisers early: Use turnaround specialists, accountants, insolvency practitioners and legal counsel to model recovery scenarios, advise on negotiations and ensure regulatory and director duty compliance.

- Improve governance and management capability: Strengthen board oversight, bring in experienced operational or turnaround leadership if needed, and set clear responsibilities and timelines for recovery actions.

- Communicate transparently with stakeholders: Maintain clear, honest dialogue with staff, creditors, suppliers and customers to preserve trust and secure cooperative solutions.

- Monitor KPIs and set trigger points: Implement tight management reporting focused on cash burn, margin, customer metrics and debt servicing; define milestones that guide further action or escalation.

- Document decisions and manage director risk: Keep contemporaneous records of key decisions and the basis for them to demonstrate that directors acted reasonably and in good faith under fiduciary duties.

Taking prompt, structured steps can sometimes rescue a struggling business; in other cases, early, controlled exit strategies preserve value for stakeholders and limit personal exposure for directors. The critical lesson is to act early, seek expert help and focus relentlessly on cash, customers and credible options for restructuring or orderly exit.