Ultimate Guide to Liquidation

Part 1: What is Liquidation?

1. Introduction

The liquidation or winding up of a company is the final step in ‘ending’ the life of a company. It refers to the final stage of realising a company’s remaining assets and distribution to creditors, according to a set hierarchy of ‘priority creditors’. It can occur both when a company is able to pay its debts (i.e., is ‘solvent’), and when it is chronically unable to do so (i.e., it is ‘insolvent’).

This ‘Ultimate Guide to Liquidation’ is split into three parts. This part, ‘Ultimate Guide to Liquidation Part One: What is Liquidation’, explains in detail the process of liquidation in Australia. This includes:

- The definition of liquidation;

- The key elements of the main types of liquidation: members’ voluntary liquidation (MVL) and creditors’ voluntary liquidation (CVL);

- The simplified liquidation process that has been introduced for small and medium-sized enterprises (SMEs);

- How liquidation compares to other insolvency processes;

- When a voluntary liquidator should not be appointed;

- The creditor power to request information from liquidators;

- The Fair Entitlements Guarantee (FEG) scheme for employees;

In the ‘Ultimate Guide to Liquidation Part 2: Preparing for Liquidation’, we look at:

- The fact that liquidations produce little financial return for creditors in Australia;

- The steps that small and medium-sized enterprises need to take to prepare for a voluntary liquidation;

- How directors should go about choosing the right liquidator;

- The situation where the courts are appoint a liquidator over the top of an ‘11th hour’ voluntary administrator.

In the ‘Ultimate Guide to Liquidation Part 3: Responding to liquidation’, we consider:

- How liquidators go about charging fees;

- How conduct of a liquidator can be reviewed;

- The steps to take to replace a liquidator;

- What directors of a company should do to minimise the fallout from a liquidation.

2. What is liquidation or winding up?

The terms ‘liquidation’ and ‘winding up’ are often used interchangeably. However, strictly speaking, under the Corporations Act 2001 (Cth), it is the overall process of ending a company that is ‘winding up’. Liquidation, by contrast, is the specific step of turning the remaining assets of the company into cash (making them ‘liquid’). The entire process is overseen and carried out by an individual called a ‘liquidator’. However, as is common in discussion of this topic, for the remainder of this guide we use the terms ‘winding up’ and ‘liquidation’ interchangeably.

So, why would a company be wound up?

Under Australian company law, the director or directors of a company have ultimate ‘oversight’ over the company – the buck stops with them. This means, directly or indirectly, they are often the ones pushing to end a company through a liquidation process.

Other key players in the life and death of a company, are the ‘officers’ and the ‘members’. Officers manage, and carry out day-to-day business operations on behalf of directors (for example, the CEO and CFO are usually officers). ‘Members’ typically own shares in the company, and make decisions on important matters, such as changes to the company constitution and decisions to wind up a company. This is achieved via ‘special resolutions’ of the members.

Directors, officers and members all have rights and obligations under legislation, regulations, company constitutions and by-laws. The reality for SMEs (businesses with less than 200 employees), is that the directors, officers and members are the same people or at least members of the same family.

There are many reasons why directors of an otherwise successful company may wish to end that business by appointing a qualified individual (a liquidator) to finalise the company’s affairs and liquidate its remaining assets: the legal procedure known as ‘liquidation’. For example,

- Sale of business through the sale and purchase of assets (as opposed to the sale of a business through the acquisition of shareholding) and the existing company no longer trading;

- The purpose for the existence of the company has ceased;

- A restructure of a group of companies whereby a subsidiary is voluntarily wound up.

At other times, the business may not be going so well. It may be insolvent, or on the brink of insolvency. At this point, directors are forced to seriously question the continued existence of the company. This is because:

- Directors can be found personally liable for continuing to trade while insolvent;

- Directors could have personal liability for tax debts via a ‘Director Penalty Notice’ issued by the Australian Tax Office.

Liquidation is not the only formal legal mechanism for ending the existence of a company: Companies can also be de-registered. However, while it is a relatively straightforward process, the following conditions must be met before doing so:

- All members must agree to doing so;

- The company must no longer be trading;

- Assets must be worth less than $1,000;

- There must be no outstanding debts or liabilities;

- The company must not be involved in any outstanding court proceedings; and,

- The company must have paid all outstanding fees and penalties.

As it is rarely the case that a recently trading company will be in this position, a voluntary liquidation is usually a necessary first step towards de-registration of the company.

For more information on this process see the Australian Securities & Investment Commission’s How to apply for voluntary deregistration.

If directors do not take seriously the decision to end the company and the question of solvency, there is a risk that a court will find them insolvent, and they will be subject to a compulsory liquidation. When this occurs, the court appoints a liquidator to supervise the winding up of the company by application of the creditors, members, the liquidator or a regulator.

3. Voluntary liquidation and insolvency

There are two main types of voluntary liquidation: a members’ voluntary liquidation (‘MVL’) and a creditors’ voluntary liquidation (‘CVL’). There is also a special type of CVL called a ‘simplified liquidation’ which is discussed in further detail in section 8 of this article.

Under section 494 of the Corporations Act 2001 (Cth), an MVL requires that a majority of directors make a ‘declaration of solvency’. If directors consider that the company is insolvent, and they seek to liquidate, they must initiate the CVL process, rather than the MVL process.

The question of solvency/insolvency is not just about which kind of liquidation must be carried out, however. It also impacts on the personal liability of directors for insolvent trading, and the possibility of another formal insolvency appointment such as a ‘voluntary administration’.

In light of the importance of solvency and insolvency, what exactly is the difference?

Section 95A of the Corporations Act 2001 (Cth) defines solvency and insolvency as follows:

- A person (including a company) is solvent if, and only if, the person is able to pay all the person’s debts, as and when they become due and payable.

- A person who is not solvent is insolvent.

According to the decisions of Courts (‘common law’), there are two tests for insolvency.

- The cash-flow test: assesses the ability of a company to pay its debts (or sell its assets fast enough to pay its debts) as they become due and payable;

- The balance sheet test: assesses the solvency of a company in reference to the total external liabilities against the total value of company assets. If liabilities exceed assets, the company is insolvent.

The cash-flow test is the principal test used by the Courts because it follows more closely the section 95A definition above. It requires an analysis of:

- The company’s existing debts;

- Whether the company’s debts are payable in the near future;

- The date each debt will be due for payment;

- The company’s present and expected cash resources; and

- The dates any company income will be received.

A key takeaway from the definition of insolvency is that it may not be obvious whether a company is solvent or insolvent. It is not enough to have a ‘temporary lack of liquidity’, there must be an ‘endemic shortage of working capital’ as per the decision in ASIC v Plymin (2003).

4. The key elements of a members’ voluntary liquidation (MVL)

As mentioned, in an MVL, the directors make a ‘declaration of solvency’ which gets the ball rolling. A meeting is then called of the members of the company to resolve by ‘special resolution’ (75% of members who attend the meeting voting in favour), to wind up the company: see section 491 of the Corporations Act 2001 (Cth).

Accompanying the declaration of solvency which is sent to members, must be a copy of the company’s statement of affairs. The declaration is required, pursuant to section 494(3) of the Corporations Act 2001 (Cth), to be:

- Made at the meeting that considers the MVL;

- Lodged with Australian Securities & Investments Commission (‘ASIC’) before the notice of the meeting is given; and,

- Made within 5 weeks of the date of the resolution to give effect to the MVL.

If these requirements are not met, the declaration of solvency will be ineffective and the winding up of the company will not be an MVL.

If the above requirements are met, and a company is successful in passing a resolution for a MVL to take place, a voluntary liquidator will be appointed. Normally, pursuant to section 532 (1) and (2) of the Corporations Act 2001 (Cth), an appointed liquidator of a company must be a registered liquidator and be independent of the company.

However, pursuant to section 532(4) of the Corporations Act 2001 (Cth), if a company is a proprietary company and the winding up is a MVL, the appointed voluntary liquidator is not required to be a registered liquidator and can be an officer of the company or other professional with the necessary expertise.

5. The key elements of a creditors’ voluntary liquidation (CVL)

A CVL, unlike a MVL, occurs when a voluntary liquidator is appointed to an insolvent company. Although a CVL is described as a ‘creditors’’ winding up, the creditors of a company are in fact unable to commence a CVL and they are usually instigated by the company director(s).

If a director forms the opinion that the company is insolvent (i.e. unable to pay debts as they become due and payable, see section 95A) and no declaration of solvency can be made, they can convene a meeting of members and resolve to pass a special resolution (75% of members after quorum is needed), to wind the company up. Creditors are not required to attend the meeting where it is resolved to wind up a company.

At the meeting, the company will appoint a voluntary liquidator. The appointed creditors’ voluntary liquidator in these circumstances, as referenced above, must comply with section 532 (1) and (2) of the Corporations Act 2001 (Cth) and be a registered liquidator and independent from the company.

Although the appointment of a creditors’ voluntary liquidator through the determination of insolvency by a director is the most common type of CVL, there are other ways that the liquidator can be appointed. These include:

- The members’ voluntary liquidator appointed under a MVL determines that the company is actually insolvent and the appointment of a creditors’ voluntary liquidator is required;

- Transition from voluntary administration to a CVL; and

- ASIC appointment.

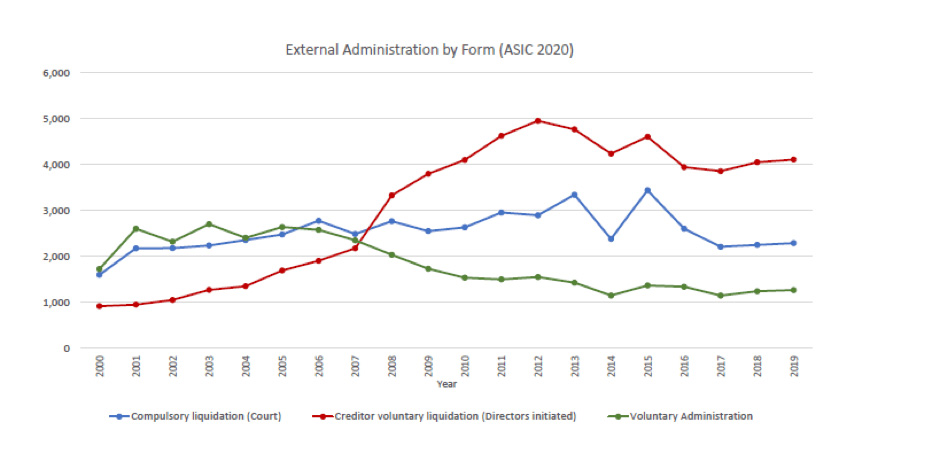

6. How MVLs and CVLs compare to other insolvency processes

Voluntary liquidation is not the only formal insolvency appointment available to directors when a company is financially struggling. Some might consider ‘voluntary administration’: This is a process where an independent professional takes control of an insolvent or near-insolvent company with the goal of coming to a successful ‘Deed of Company Arrangement’ or ‘DOCA’ with creditors to settle their outstanding claims.

The chart below compares the rates of different types of insolvency with voluntary administrations. As you can see, CVL is more-or-less four times more common than a voluntary administration.

Why is this? It might be that, by the time that a company seeks advice on a formal insolvency appointment, it is in so much difficulty that winding up is inevitable. Or, it could be that a voluntary administration is usually interpreted as a “glorified liquidation” anyway, in which case going straight to liquidation would reduce formal appointment costs.

7. Restructuring under part 5.3B Corporations Act 2001 (Cth)

It has long been suggested that the existing formal insolvency processes were inadequate in Australia, and that there needed to be tailored processes in place to support turnaround for SMEs. In response, in 2021 a new Restructuring process was added to the Corporations Act 2001, especially for SMEs. This process establishes the role of a ‘ Restructuring Practitioner’ (‘practitioner’) who oversesees formal restructuring. This process is sometimes called ‘small business restructuring’ or ‘simplified debt restructuring’. In short:

- A small business in financial difficulty approaches a practitioner to discuss a possible restructure;

- If appropriate, the practitioner advises that re-organisation is appropriate and proposes a flat fee for completing the work;

- By a resolution of the directors, the company appoints the practitioner. From this point unsecured creditors cannot take action against the company, personal guarantees cannot be enforced and protection from ipso facto clauses applies;

- The business owners/directors work with the practitioner to develop a restructuring plan. They have 20 days to do so. If satisfied, the practitioner can ‘certify’ that plan;

- Both the plan and associated documents (such as the practitioner’s fees and expenses) are sent to creditors;

- Creditors vote on whether to accept the plan and proposed remuneration and have 15 days to do so. Where more than 50 per cent of creditors by value agree to the plan, it is approved and then applies to and binds all unsecured creditors;

- Once (and if) approved, the business will continue to trade with the practitioner making the required distributions under the plan.

- If the creditors do not approve of the plan, the process ends and directors must decide whether to go into voluntary administration, or go into liquidation. Note, in many cases, the business will be eligible for ‘simplified liquidation’ (see below).

To read more about this process, see our Guide to Restructuring.

8. The simplified liquidation process for small businesses

It has been evident for a long time that Australia’s ‘one-size-fits-all’ liquidation model is inappropriate for small-to-medium sized enterprises. This inadequacy became particularly evident in the wake of the Covid-19-related economic turbulence. In response, the federal government introduced a simplified liquidation process.

In overall structure, this new process is similar to existing liquidation processes, albeit with a range of changes made to speed up and reduce the cost of liquidation. As with a standard liquidation, small businesses will be able to appoint a liquidator to wind up the company and liquidate any remaining assets to distribute to creditors. As with standard liquidations, the liquidator will still have the capacity to investigate potential wrongdoing and report to creditors.

This process is available for companies with liabilities less than $1 million, which have met their tax filing obligations and where shareholders and directors agree that it is appropriate

The liquidator can still investigate and report to creditors about the company’s affairs and inquire into the failure of the company.

Key changes from the normal CVL process include:

- Fewer situations are permitted where the liquidator is able to clawback ‘unfair preference’ payments or otherwise void transactions. In a standard liquidation, liquidators have the power to pursue certain transactions entered into by the company which conferred a preference on one or some of the creditors, or provided a benefit to a related party or creditor to the detriment of other creditors. The goal is to increase the ‘pot’ of assets available for distribution. Section 500AE of the Corporations Act 2001 (Cth), read in conjunction with Regulation 5.5.04 of the Corporations Regulations 2001 (Cth) modify the usual rules that apply to liquidators. This includes provision that the liquidator does not need to investigate nor claw back small-value transactions (less than $30,000 in value).

- An alteration to the rules around liquidator reporting. The liquidator is only required to report to ASIC about potential misconduct where there are reasonable grounds to believe there was misconduct (see section 533 of the Corporations Act 2001 (Cth)). The mandatory reporting requirement in standard liquidations is time-consuming and expensive, significantly eating into the remaining assets that would otherwise be available for distribution to creditors. In simplified liquidation, the liquidator is only required to submit a report to ASIC where there is evidence of serious misconduct;

- Removal of the liquidator’s requirement to call a meeting of creditors. In a standard liquidation, some creditors or ASIC are able to direct that a liquidator hold such a meeting. Instead of being required to convene a meeting, liquidators will be required to provide information to creditors, and put proposals to them, electronically;

- Removal of the capacity for creditors to create committees of inspection. In a regular liquidation, creditors have the capacity to appoint a committee of inspection which oversees the liquidator process and has the power to approve liquidator fees and expenses;

- Removal of the capacity for creditors to appoint a ‘reviewing liquidator’. We discuss the role of the reviewing liquidator further in the ‘Ultimate Guide to Liquidation Part 3: Responding to liquidation’ Note, the court still retains its oversight powers, so it will be able to appoint a reviewing liquidator as required;

- Simplification of the dividend and proof of debt processes;

- Technology neutrality for voting and other forms of communication.

Under certain circumstances, companies will exit the simplified liquidation process. This will occur, where the liquidator becomes aware that the eligibility criteria are no longer met. This could happen, for example, where the liquidator becomes aware of an additional creditor meaning that the company no longer has less than $1 million in liabilities.

When the company is no longer eligible for the simplified process, they are transitioned into the standard liquidation process.

9. Safe harbour restructuring

Whether a CVL, a voluntary administration or a compulsory liquidation, formal insolvency appointments usually mean the death of the business. While Restructuring Under Part 5.3B of the Corporations Act 2001 (Cth) offers some chance of helping SME directors turn their business around, it still has limits on its scope (namely, a higher limit of $1 million in liabilities).

There is another mechanism available for companies that seek to avoid a formal insolvency appointment. Under section 588GA of the Corporations Act 2001 (Cth) it provides that the duty of a director not to trade while insolvent does not apply if:

- at a particular time after the director suspects insolvency, the director develops a course of action that is reasonably likely to lead to a better outcome for the company; and

- the company debt is incurred in connection with the course of action.

10. When you shouldn’t appoint a voluntary liquidator – a checklist

We suggest that, before initiating the process for appointment of a voluntary liquidator, you consider the following checklist and do not appoint a voluntary liquidator if one of the criteria applies:

- As outlined above, if you plan to continue trading afterwards

- If you have uncommercial transactions or unfair preference claims that can be made against you. In these cases, you need to see a lawyer first;

- If you have a directors’ loan account owing;

- If you haven’t considered an informal restructure first as an option;

- If you are a SME director and you have not considered the possibility of appointing a restructuring practitioner and going through a formal restructuring process;

11. What is the creditor power to request information from liquidators?

In addition to the poor outcomes of liquidation for directors and creditors, a common complaint about liquidation in Australia has been the lack of transparency in the process. Many creditors have felt like there is inadequate disclosure by liquidators of key information. Prior to 2016, creditors were limited in their ability to hold liquidators to account via reporting and information gathering. This was improved in 2016 when a new insolvency framework was introduced to ensure that creditors have a right to request reports, documents and information from liquidators (whether individually or as a group).

This has been seen as an improvement on the pre-2016 framework which left creditors largely in the dark about key liquidation issues. We explain this power to request information below.

The problem: lack of disclosure

When a company is wound up, creditors do not (usually) appoint the liquidator, even though the liquidator is required to act in the interests of the creditors. In light of this, creditors often end up unsatisfied with the liquidation process. Their frustrations include:

- An overwhelming feeling of impotence in the liquidation process. Creditors may find their inquiries with liquidators unanswered;

- Creditors perceive liquidators as acting as an effective monopoly. With terms of engagement so common across liquidators, creditors don’t feel they can easily appoint a better alternative, and they know they are practically impossible to replace;

- Slow liquidations – the timeframe for liquidation is 1-2 years.

In this section, we are focused on the information-gathering power available to creditors to manage their frustration with creditors. However, it is worth noting that there are other mechanisms available to creditors for supervising liquidator conduct, including:

- removal of liquidators via a resolution of creditors;

- court applications for replacement of a liquidator;

- appointment of a ‘Reviewing Liquidator’;

- appointment of a committee of inspection.

The 2016 Rules

Creditors may now request their liquidator for information, reports or documents under Division 70-40 (when acting collectively by resolution) or 70-45 (when acting individually) of the Insolvency Practice Schedule (Corporations). This right applies to creditors in a creditor’s voluntary winding up and ‘members’ in the case of a members voluntary winding up.

While our focus in this article is on the power of creditors to acquire information from liquidators, these provisions also apply in the case of voluntary administration.

Under 70-40(2) and 70-45(2) of the Insolvency Practice Schedule (Corporations), a liquidator must comply with this request except where:

- The information, report or document is not relevant to the liquidation;

- It would breach their duties as a liquidator;

- It would otherwise be unreasonable to do so.

The Insolvency Practice Rules (Corporations) 2016 set out the conditions under which a liquidator may hold that it is not reasonable to comply with the request. We will look at this power later in the article.

Pre-2016 creditor information powers

Prior to the introduction of the Insolvency Practice Schedule (Corporations) and Insolvency Practice Rules (Corporations) 2016, what options were available for creditors who required information? The key mechanisms were:

- Compulsory reporting processes. These were concerned primarily with directors reporting to liquidators and ASIC (e.g. in the Report as to Affairs (RATA) now largely replaced with the Report on Company Activities and Property (ROCAP)). While liquidators were expected to provide written reports to creditors, this often didn’t happen;

- Right to view the liquidator’s books. Liquidators had (and still do) a right to inspect the liquidators’ books, which in turn must be up-to-date and accurate. This requires significant effort on behalf of the creditor and is not a general right to information;

- Powers of the committee of inspection. Creditors can choose to appoint a ‘Committee of Inspection’ early in the liquidation process who represent the creditors and can direct the liquidators to act in various ways. Note, however, that the liquidator is not generally bound by the directions of the committee of inspection.

How is the power to request information useful?

The limits of committees of inspection and existing reporting processes meant that, in reality, creditors were limited in their ability to supervise the liquidation process. In addition to improving the tools available to creditors, the new right seeks to:

- Enable creditors to ensure that liquidators are acting in their interests as required to by law;

- Enable creditors to supervise the liquidator’s costs themselves.

- If there is a prospect of future litigation, provide an alternative to discovery in expensive court action. This was confirmed in In the matter of 1st Fleet Pty Ltd (in liquidation) [2019] NSWSC 6.

Liquidator’s right to refuse

The creditor’s right is only a right of request. As set out above, there are specific grounds under which the liquidator can refuse to comply under the Insolvency Practice Rules (Corporations) 2016. The most significant of those grounds for refusal are set out in 70-10 of the Insolvency Practice Rules (Corporations) 2016. A liquidator can refuse the request if:

- complying with the request would substantially prejudice the interests of one or more creditors or a third party and that prejudice outweighs the benefits of complying with the request;

- the information is privileged;

- disclosure could be a breach of confidence;

- insufficient available property to comply with the request;

- the information, report or document has already been provided; or

- the information, report or document is required to be provided under the Corporations legislation within 20 business days of the request being made; or

- the request is vexatious.

These grounds significantly limit the liquidator’s power of refusal. In the matter of 1st Fleet Pty Ltd (in liquidation) [2019] NSWSC 6, the court overruled a liquidator’s decision to refuse to provide information on the grounds that they had already provided that information to the committee of inspection. As the prior provision of the information to another party is not a specified ground for refusing to provide information, the liquidator could not refuse on those grounds.

Conclusion – the power of the power to request information

The new power for creditors to request information for liquidators puts significant power back in the hands of creditors. While liquidators do have the power to refuse to provide that information, the grounds for refusal are significantly limited.

12. What is the Fair Entitlements Guarantee (FEG) scheme?

As discussed, the returns for unsecured creditors in liquidation in Australia are poor. In response there is a scheme to support employees known as the Fair Entitlements Guarantee (or ‘FEG’) scheme.

The FEG Scheme, previously known as the General Employee Entitlements and Redundancy Scheme (GEERS) is available to all eligible employees to ensure they get (some) of what they are entitled to. The FEG Scheme provides for:

- Unpaid wages of up to 13 weeks (capped at a maximum weekly wage, currently set at $2,451);

- annual leave;

- long service leave;

- payment in lieu of notice of termination set at a maximum of 5 weeks;

- redundancy pay of up to 4 weeks per full year of service.

Note, that the FEG Scheme does not cover all employee entitlements. It does not cover:

- superannuation;

- reimbursement payments;

- one-off or irregular payments;

- bonus payments;

- non-ongoing or irregular commissions.

For more information on the FEG Scheme see the Fair Work website.

The FEG scheme, as a scheme of last resort, is intended only to apply where there are insufficient assets to pay out employee entitlements. Note also that there are eligibility restrictions. The restrictions include the scheme not applying to contractors and those who have been directors of the company within the last 12 months of the company, among other conditions.

There has been a concern in recent years that companies have been misusing the FEG Scheme, including the occurrence of ‘illegal phoenix activity’, where assets have been transferred out of the company prior to insolvency which would have otherwise been used to pay employees their entitlements.

Contractors are not employees

As contractors are not employees, they are simply ordinary unsecured creditors when it comes to the winding up of the company. This means that (a), they have no priority in liquidation and (b), they have no access to the FEG Scheme. This means that the following question becomes crucial: is a given individual an employee or a contractor? The answer does not depend simply, on whether there is an employment agreement or contract in place. There is no hard-and-fast rule determining whether a given person falls into one category or the other. However, for tax and superannuation purposes, the Australian Tax Office (‘ATO’) considers the following factors determinative:

- Ability to subcontract/delegate: An employee generally cannot subcontract/delegate their work, but a contractor can;

- Basis of payment. An employee is paid either for the time worked, a price per item or activity or a commission, whereas a contractor is paid for a result achieved;

- Equipment, tools and other assets. Employees are usually supplied equipment and tools whereas contractors usually supply their own;

- Commercial risks. The worker takes no commercial risks as the business is responsible for the work done and rectifying it. Contractors take commercial risks and are responsible for rectifying any defects in work completed;

- Control over the work. The business has the right to direct employees in how they get their work done, whereas a contractor has considerable freedom in how they complete the work;

- The worker is part of the business whereas the contractor operates an independent business and is free to accept or refuse additional work.

For further information check on the ATO website.

Options for contractors

As the majority of liquidations in Australia result in very few assets remaining to distribute to unsecured creditors, this will often mean unsecured creditors walk away from a liquidation empty-handed. In light of this, it is important that contractors take into account this commercial risk when they enter into a contract. In addition, it may be possible in some cases for contractors to secure their debts through registration of a security interest (e.g. over the equipment of the debtor company).

Once winding up is underway, what options are open to the contractor to get what they are owed? Options for contractors are limited, but matters worth considering include:

- Making a claim of ‘sham contracting’. Considering the factors outlined in section three, ‘contractors’ might consider whether they are in fact employees and therefore entitled to priority in liquidation and/or access to the FEG Scheme.

- Using creditors’ remedies to increase the pool of remaining assets. An ‘unfair preference’ claim might be made where one creditor (such as a contractor) has been discriminated against in favour of another contractor. This can occur when the company has made payments to one creditor prior to winding up where the company was already insolvent.

14. Conclusion of part one

To summarise the liquidation process as discussed in part one of this ‘Ultimate Guide to Liquidation’:

- The decision whether or not to appoint a voluntary liquidator (or initiate the process), is a serious one for directors and it needs to be pursued with caution;

- The type of liquidation that is initiated, MVL or CVL, depends on whether the company is solvent (and whether directors are confident to make a declaration to that effect);

- A key difference between MVLs and CVLs is that the liquidator in an MVL is cheaper;

- Voluntary liquidations are much more popular than voluntary administration, perhaps reflecting the fact that once a business is insolvent it is often too late for a voluntary administration to be of value.

- The simplified liquidation procedure may increase the likelihood of returns for unsecured creditors of small businesses.

In order to avoid liquidation, businesses might consider:

- Whether safe harbour protections might be employed to pursue informal restructuring solutions ;

- Whether they are eligible for Restructuring under the Corporations Act 2001 (Cth) or voluntary administration.

Key details of the liquidation scheme in Australia that all directors and creditors should be aware of includes:

- The Fair Entitlements Guarantee (FEG) scheme;

- The power of creditors to request information from liquidators;

Part 2: Preparing for Liquidation

1. Introduction

In part one, we considered the question ‘What is liquidation?’. We explained all the main types of liquidation in Australia (members’ voluntary liquidation, creditors’ voluntary liquidation and simplified liquidation), and briefly looked at some of the alternatives that are available (such as the safe harbour and restructuring under the Corporations Act 2001 (Cth)).

In this part, part 2, we look at how to prepare for liquidation. We begin by looking in greater depth at the shortcomings of liquidation (the returns for creditors are generally very low), before looking at general steps directors can take to prepare for liquidation, how to choose the right liquidator, and how the court will deal with attempts of directors to prevent winding up with the appointment of an ‘11th hour’ voluntary administrator.

In the next part, part 3, we will look at how businesses can best deal with the aftermath of liquidation.

2. Unsecured creditor prospects in liquidation

In liquidation, the company is wound up, any remaining assets are realised and distributed to creditors. But who gets priority for the remaining assets? Priority for the proceeds of the winding-up goes to secured creditors. Even among secured creditors, some interests, such as a Purchase Money Security Interest (‘PMSI’) have ‘super-priority’ over other secured interests.

For unsecured creditors, creditors who do not have a registered security interest in the assets of the company, funds are distributed in order of priority as set out in section 556 of the Corporations Act 2001 (Cth):

- The costs and expense of the liquidation, including liquidators’ fees;

- Outstanding employee wages and superannuation;

- Outstanding employee leave of absence (including annual leave and long service leave);

- Employee retrenchment pay;

- Remaining unsecured creditors.

Given the order or priority, what are the prospects of the remaining unsecured creditors getting a return? While there is frustratingly little recent data on the average return of insolvency for unsecured creditors, when Parliament looked into this in 2023:

- Personal bankruptcy statistics indicated average returns for unsecured creditors. at 1.6 cents in the dollar. We can assume that corporate insolvency is not much better;

- The dividend to creditors was estimated to be zero cents per dollar for 85 to 92 per cent of reported liquidations over the previous 15 years

Note also that these statistics overstate the prospect of a return for the median creditor. Outcomes are skewed by a few larger businesses leaving more significant pay-outs. In our experience, the expected return for the median unsecured creditor is zero cents on the dollar. As the overwhelming majority of windings up end up in Australia are small-sized and family businesses with a small asset base, it is unsurprising that zero assets are leftover in so many cases.

It is also worth observing that the financial loss from liquidations is not just a loss to individual creditors but constitutes a significant loss to taxpayers as well; the Australian Tax Office (ATO) is almost always the largest unsecured creditor and yet they have no priority and so are usually unable to recover unpaid taxes.

Several years ago, the Australian Small Business and Family Enterprise Ombudsman conducted an inquiry into the effect of insolvency practices on small businesses and made a range of recommendations. You can read more about it here.

It is worth noting that the new simplified liquidation process (see Part One) is intended to substantially reduce the cost of liquidation for small businesses by streamlining the liquidation process. While there do not appear to have been any studies released, anecdotally, it does not appear that many businesses have taken part in the simplified liquidation process thus far.

3. Options for creditors to rein in the costs of the liquidation

In response to a perception that insolvency practitioner fees are too high and are having a negative impact on liquidation outcomes, a range of reforms were introduced in 2016, including enhanced powers for creditors to approve liquidator remuneration and expenses and the appointment of a ‘reviewing liquidator’. In the liquidation process, creditors need to consider.

- The remuneration and expenses approval process. In the case of a creditors’ voluntary liquidation (CVL), remuneration and fees must be approved by the creditors themselves, a committee of inspection, or the Court. If fees are not settled by either resolution of creditors or the committee of inspection then they must be set by the Federal or Supreme Court. We discuss this in greater detail in part three of this series.

- Appointment of a Reviewing Liquidator. Creditors also have the option of appointing a ‘Reviewing Liquidator’ who is a registered liquidator appointed to review the remuneration and costs charged. There are two mechanisms for appointing a reviewing liquidator:

- by a resolution of creditors. If this occurs, the costs of appointing the reviewing liquidator are added to the costs of liquidation;

- without a resolution, but with the consent of the liquidator. If this occurs, the applicant creditor must bear the costs of appointing the reviewing liquidator.

This Reviewing Liquidator can only look into:

- remuneration approved in the prior six months; and

- costs or expenses incurred during the previous 12-month period.

We discuss the role of the Reviewing Liquidator process in detail in Part 3. It is worth noting that, as the cost of the Reviewing Liquidator is added to the costs of the liquidation, this can further reduce the pool of money available to unsecured creditors. If the liquidator doesn’t have sufficient funds then the creditors may be called upon to provide an indemnity.

Another option for creditors seeking to rein in excessive liquidator remuneration and expenses is to make a court application. Under section 447A of the Corporations Act 2001 (Cth), the court has broad powers to make orders as it sees fit in relation to liquidation. This application allows creditors, others with a financial interest and directors apply to the court for an order:

- For a determination in relation to any matter related to the liquidation;

- An order that an individual be replaced as the liquidator;

- Remuneration orders.

As always with court proceedings, this will be an expensive and time-consuming process. This is why creditors aren’t enthusiastic about Court application.

4. Alternatives to liquidation for creditors

Given the poor prognosis for unsecured creditors, what other options do they have available to them? We already mentioned in the first section of this article that creditors could consider issuing a statutory demand for payment in order to prompt the debtor company into payment.

Other possible options include:

- Voluntary Administration. This process that is usually initiated by the directors of the company, seeks to arrive at a ‘Deed of Company Arrangement’ (DOCA) by agreement of creditors that will provide them with a better outcome than proceeding directly to liquidation. This process has a chance of being more succesful with larger companies who are ineligible for small business restructuring (see discussion below).

- Schemes of arrangement. These relatively uncommon arrangements, regulated under Pt 5.1 of the Corporations Act 2001 (Cth), are binding, court-approved agreements, allowing for the reorganisation of the rights and liabilities of members and creditors of a company. Note, however, that as this is a court-supervised process involving significant input from the ASIC, it is by no means a cheap or quick option. Note also that, this option is limited to big corporates.

- Restructuring under the Corporations Act 2001 (Cth). This process, introduced in 2021, involves a special kind of insolvency practitioner, a Restructring Practitioner, being appointed to a small business during insolvency. The restructuring practitioner is appointed to work out a restructuring plan and get it approved by creditors. Note, unlike voluntary administration, the directors of the company remain in control of the company (‘debtor in possession’) throughout the process. This process is only available for companies with liabilities of $1 million or less.

- Informal mechanisms. Another possibility is for creditors to consider negotiating directly with the company without putting them into liquidation. While, in some cases, creditors may appreciate the satisfaction in ‘punishing’ debtors through liquidation, the non-liquidation is likely to lead to a better financial outcome for the creditors. This is ruled out however when creditors don’t have sufficient trust in place.

5. The final verdict on the success rates of liquidation

All-in-all, forcing a liquidation is often not a cost-effective and efficient means for a creditor to get a return on what they are owed. There has been a significant rise in CVLs and a reduction in court-appointed liquidations in recent years. This, perhaps, recognises both the expense in creditors going through the court process, as well as a tendency for existing liquidation processes to benefit the debtor company and liquidators more than creditors. For example, it is likely that directors often use CVL process to avoid their own liability in many cases, such as personal liability for tax debts.

In light of this, it is worth non-director creditors exploring other options, besides liquidation, in order to get the best chance of a return on their debt. Often an informal negotiation process for repayment of the debt may be the best option for creditors. Steering clear of bad payers and clients with poor credit is a sensible prescription to avoid liquidations. Credit insurance is another protection option. Once those informal options have been explored, formal turnaround options like Restructuring or voluntary administration may be appropriate before resorting to liquidation.

6. Prepare for a voluntary liquidation

The terms ‘liquidation’ and ‘winding up’, just like the terms ‘bankruptcy’, ‘tax office’ and ‘new season of Married at First Sight’, carry a degree of anxiety. But they shouldn’t. Liquidation, or the ‘winding up’ of a company, can happen for many different reasons: it does not necessarily mean that the business is broken beyond repair. Liquidation has a different impact on a company depending on how, and why, it was initiated. Matters to consider include:

- Has a winding up petition been filed in court with respect to the company? If so, depending on whether you can challenge the petition in court, the company may be wound up and liquidated, whether you like it or not. This is an ‘involuntary’ or ‘compulsory’ liquidation;

- Is the company financially healthy, but no longer fit-for-purpose, or superfluous for some reason? In this case you may be able to consider a members’ voluntary liquidation (‘MVL’);

- Is the company insolvent, or likely to become insolvent? A company is insolvent when it is unable to pay its debts as they fall due and payable. At this point, voluntary administration, small business restructuring, or CVL become possible options.

Let’s consider this third option in greater detail. As mentioned before, in voluntary administration, an independent professional is handed the reins by the directors, in an attempt to negotiate a DOCA for the payment of creditors. In Restructuring an independent professional is appointed to support directors (who remain in control) by coming up with a plan to restructure the company, which creditors must then approve. In a CVL, a liquidator is appointed in order to terminate a company and realise its remaining assets for the benefit of creditors.

The appointment of either the voluntary administrator, Restructuring Practitioner or liquidator also has the legal benefit stopping all action for debt recovery from creditors. It is worth noting that while liquidation does end the life of a particular company, it doesn’t necessarily mean the end of the ‘business’, broadly conceived.

When might voluntary liquidation be a good idea?

If your business is insolvent, or likely to become insolvent, you need to take immediate action. If you don’t take some kind of action, you may be in breach of your duty as a director to prevent insolvent trading of the company (see section 588G of the Corporations Act 2001 (Cth)). What are the possible actions you might take?

- You could sell business assets to third parties to pay down debt;

- You could appoint a voluntary administrator;

- You could consider a formal debt restructuring by a Restructuring Practitioner (where an eligible small business);

- You might consider an informal ‘work around’, such as securing rescue finance, an extension of terms from suppliers, or a payment plan with creditors, in order to bring the company definitively back into solvency.

There may be situations where none of the above possibilities are appropriate. For example, where there is no longer a valuable business model underlying the business at all. In that case, it may make sense for directors to appoint a liquidator immediately.

It may also be sensible to appoint a liquidator where creditors are likely to pursue the winding up of the company via a compulsory liquidation. This way, directors can take positiver action to initiate an appointment process.

Prepare for a voluntary liquidation: preliminary assessment of the books

The first step is to get the books in order to get a clear picture of your financial situation. This will determine whether formal insolvency options should be pursued, or whether you still have informal options open to you.

When looking at your financials, you need to consider:

- Your bookkeeping systems. Without having an accurate and up-to-date record of your revenue, expenses, assets and liabilities, you will have little idea whether your company is solvent or insolvent;

- Assess your cash position. Look at your current ratio (current assets/current liabilities), quick ratio (liquid current assets/current liabilities) and operating cash flow ratio (operating cashflow/current liabilities), to determine whether you have the cash coming into keep paying your bills;

- The state of your accounts payable. Note, in particular, whether any statutory demands for payment of debt have been made, and whether you can cover your upcoming employee entitlements and tax liability;

- Review asset structuring. Does the company in difficulty actually own the relevant assets (or are they leased from another entity, for example)? This means you can assess which assets would need to be liquidated if a liquidator is appointed;

- What is the state of the directors’ loan accounts? It is common for directors of small-to-medium sized enterprises to draw down on the business through a loan account, rather than be paid entirely through a salary. There is the potential for this loan to be called in, when a liquidator is appointed, so you need to work out what your position is here. There is also issues with the calculation of interest for valid ‘Div 7A’ loans that the company accountant will need to include in the financials.

Prepare for a voluntary liquidation: solvency review

Once you have informally assessed your finances, you need to get a professional to conduct a solvency review. This is crucial, because if the company is solvent, then this has an impact on which options are available to directors to save the business. Directors of a solvent company can initiate an MVL rather than a CVL. The advantage of this option is:

- It is likely to be cheaper, as there is no need to appoint a registered liquidator;

- Members (i.e. shareholders) get to control the direction of the liquidation;

- The liquidator need not be independent of the company;

If, after a solvency review, the company is determined to be insolvent, an MVL will not be an option. At this point, you need to consider other options, including:

- Voluntary administration. Like the appointment of a liquidator, the appointment of a voluntary administrator will halt any claims against the company, while the voluntary administrator attempts to negotiate a ‘deed of company arrangement’ with the creditors.

- Use the ‘safe harbour’ under section 588GA of the Corporations Act 2001 (Cth), to enable an informal workaround to insolvency. This could include negotiating more favourable payment terms with creditors or accessing rescue finance;

- If eligible, initiate the debt restructuring process for small businesses (i.e. small business restructuring);

- Immediately initiate a CVL. This will mean a halt to all creditor proceedings against the company. However, this will also mean the end of the business as a going concern.

Prepare for a voluntary liquidation: assessing your liability before appointment of the liquidator

An important consequence of a liquidator being appointed is that the liquidator is empowered to investigate the affairs of the company. This means that they can question, and potentially take action, with respect to prior actions of directors. Directors need to consider the possibility of:

- Uncommercial transactions. Transactions are deemed uncommercial if it is deemed that a reasonable person, considering the benefits and detriments of a given transaction, would not have entered into it. An uncommercial transaction can only occur where insolvency can be proven at the time of the transaction;

- Unfair preference claims. These happen where a creditor is paid for something that they are owed, which gave them an advantage over other creditors, where that creditor knew or ought to have known the company was insolvent;

- Unreasonable director-related transactions. These transactions are ones where directors enter into transactions that a reasonable person in the director’s circumstances would not have;

- Creditor defeating dispositions. These transactions are commonly referred to as ‘illegal phoenix activity’. They occur where there is a “disposition of company property for less than its market value (or the best price reasonably obtainable) that has the effect of preventing, hindering or significantly delaying the property becoming available to meet the demands of the company’s creditors in winding-up.”

In general, directors need to take a strategic approach to the payment of their debts before the CVL commences. In particular, they should look at whether any debts which have director personal guarantees attached can be paid. Note however that in doing so, legal advice must be sought to ensure that legal liability is not incurred for any of the matters set out above. Restructuring an insolvent business with asset transfers requires expert professional opinion to ensure that none of the above illegal or voidable transactions are undertaken.

Director action during the voluntary liquidation process

Once the liquidator is appointed, directors are obligated to support the conduct of the CVL in various ways. This includes:

- advising the liquidator on the location of company property;

- providing books and records;

- providing a written report about the company’s affairs within five business days;

- meeting with the liquidator to help with their inquiries, as reasonably required;

- if requested, attending a creditors’ meeting to provide any required information.

The CVL will come to an end once the liquidator has realised and distributed the company’s remaining assets and lodged a final account with the ASIC. Three months after this point, the company will be de-registered.

Key takeaways when preparing for voluntary liquidation

When preparing for liquidation, company directors should consider the following factors:

- Liquidation could be caused by issues not related to insolvency. Not all liquidations imply something has gone wrong in a company;

- Before considering appointing a liquidator, directors need to take stock of their financial situation. This means basic bookkeeping, looking at key financial ratios and assessing the state of creditors;

- The next step is getting a professional opinion on the solvency of the company. This will determine which type of liquidation is available (MVL, CVL or simplified liquidation);

- Once it has been determined that a liquidator should be appointed, directors need advice in order to carefully assess their legal liability;

- Once a CVL is underway, directors are required to support the liquidator in various ways as required by law.

7. How do you choose the right liquidator?

The company liquidation process (a CVL for insolvent companies) can be a long and winding road for company directors. While directors might get to appoint the liquidator, they don’t owe the directors or owners any legal duties, so it is best to pick an ethical and commercially-minded liquidator. The size and culture of the liquidator’s firm should be carefully considered because you will likely be dealing with them a lot.

Why does it matter to pick the right liquidator?

- Although directors may appoint the liquidator in a creditor’s voluntary liquidation, the liquidator has the legal duty to act for the creditors;

- While the liquidation is running, the directors will be subject to investigations by the liquidator and they may be sued to recover funds or as punishment for breaching their duties to the company;

- The liquidator may communicate with the media about the liquidation and the director’s conduct;

- The liquidator has a legal duty to report impropriety to ASIC and/or the police;

- It is highly unlikely that the liquidator can be removed by the directors – so selecting a liquidator is a decision that is probably irreversible.

Take-away for directors: Overall, a company liquidation is stressful – so why pick someone unless they’re the best person for the job?

When do you appoint a liquidator?

When a company is insolvent and the directors decide to cease trading, a voluntary liquidator should be appointed.

If the directors put off appointing a liquidator for too long, they may increase their risk of facing the following consequences:

- A director’s penalty notice being issued by the ATO to pierce the corporate veil (read our blog post about DPNs – Director Penalty Notice for further information);

- Creditors taking action to wind up the company themselves and appointing their preferred liquidator;

- An action against the directors for breaching their legal duties by trading whilst insolvent:

Consideration 1: The size of the firm is important

The first consideration for choosing a liquidator is to work out the optimal firm size for the type of appointment.

What type of liquidator firms are there?

- Large-sized firms: firms with greater than 20 partners, big city offices and sophisticated support services

- Medium-sized firms: firms with more than 5 partners, large offices and limited support services

- Small firms and sole practitioners: firms with 1-3 partners, a single office and no support services

What are the capabilities of liquidator firms?

- Large-sized firms: Undertaking large liquidations for companies with more than 200 employees with IT and forensic accounting support

- Medium-sized firm: Undertaking small and medium-sized appointments (companies with less than 200 employees) but without sophisticated IT and forensic accounting support

- Small firms and sole practitioners: Largely undertaking small business liquidations (less than 20 employees) but without the capability to deal with IT issues or forensic accounting issues

What are the ideal referrers for liquidator firms?

- Large-sized firms: Banks and private equity funds

- Medium-sized firms: Large accounting firms and large law firms

- Small firms and sole practitioners: Small accounting firms, small law firms and consultants

The key limitation is usually economic because the larger a liquidator’s firm is, the more expensive it will be to engage them. However, in larger liquidations, a larger firm may be necessary to get a better quality administration process and a faster result. In any liquidation, it is likely that the directors want the business closed down and to have their record of conduct given a “tick” by an investigating liquidator. Further, if the key creditor is a bank or large financier, they may require the appointment of a liquidator who is on their panel.

The key downside of a smaller liquidation firm is that they will be slower in achieving their deliverables. However, they will be a lot cheaper. If a company liquidation has less than $200,000 in assets then directors should look to a smaller firm or sole practitioner as being fit for purpose.

Take-away for directors: Appoint a firm that is the right size for the work that needs to be done in your liquidation.

Consideration 2: The culture of the firm

Organisational psychologists will tell us that culture is “hard-wired” into an organisation. This means that you can’t expect any organisation to change its values or methodology because you ask them to. Culture is something that permeates “top-down” in an organisation, so the partners will give you the strongest indication of the firm’s overall culture. You’ll also need to work out ways to test the culture of the firm. Some ways to test their culture and values could include asking yourself:

- Do they offer you water in the board room?

- Do they show an interest in you?

- Do they contribute to society, e.g. by supporting a charity or through other CSR schemes? and

- Are family values important to them?

Take-away for directors: Appoint a firm that has appropriate values.

Consideration 3: Professional fees

Like in any business transaction, the price of the services on offer is a critical consideration. If possible, company directors may try to persuade a liquidator to take the appointment on the basis that they get paid from the liquidation of the assets in the company itself. If the company is assetless, then they may be asked for advance payments, or to promise to indemnify the liquidator for a sum between $5,000-$100,000.

The proposition that a liquidator will take on an appointment for a fixed fee is wrong. It is wrong because approval from creditors can lead to a fee adjustment.

Take-away for directors: See if you can find a liquidator that will take the appointment with no upfront fee.

Consideration 4: Experience is paramount

Experience is essential for any team that supports a liquidator because the actual appointee’s time is limited. Their team can only gain confidence and skill through working on liquidations similar to your own. The same applies to the liquidator who is specifically appointed to your matter.

Take-away for directors: Only appoint experienced liquidators with good teams.

Consideration 5: Ethical and hard working

Company directors should only engage hard working and ethical liquidators. This type of liquidator is the most likely to be able to negotiate successfully through the difficult liquidation process.

Take-away for directors: Engage only ethical and hardworking liquidators because they are more likely to follow through.

Consideration 6: Commercially minded

Liquidators need to make commercial decisions quickly.

The types of commercial decisions that liquidators need to make include:

- Determining the process for selling assets and the best price that can be obtained for those assets

- Whether to commence proceedings against creditors to recover unfair preference claims

- Whether it is feasible to commence insolvent trading actions or undertake any other claw-back actions against the directors

- Whether to reverse any pre-appointment transactions that the directors entered into (i.e. phoenix activity)

- How long to continue a liquidation and whether to initiate extensive investigations into the director’s conduct through examination hearings in open court

Directors have no interest in engaging an intransigent liquidator who undertakes actions that only have the benefit of increasing their chargeable hours without any tangible benefit for creditors or other stakeholders.

Take-away for directors: Engage a commercially-minded liquidator.

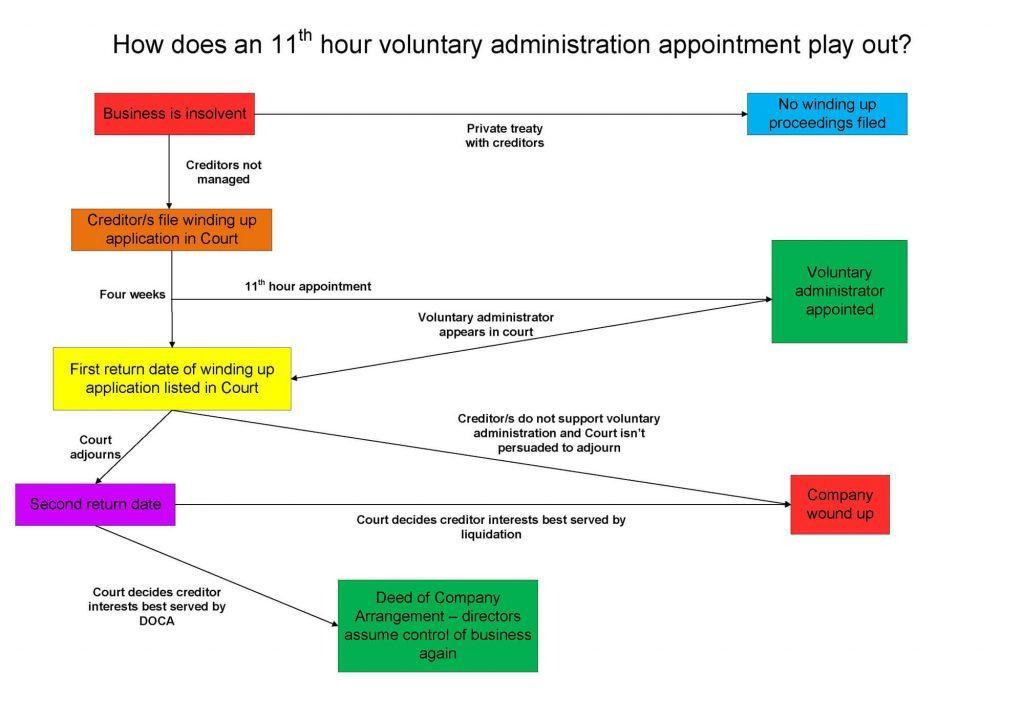

8. Will a Court appoint a liquidator over the top of an 11th hour voluntary administrator?

Company directors are sometimes persuaded to appoint voluntary administrators while there is a winding up petition before the Court to liquidate the company. In this situation, the voluntary administrator/s will need to appear in Court and convince the Judge it is in the best interests of creditors to allow the voluntary administration to continue (rather than immediately winding up the company).

The key issue for directors is that it is not a relevant consideration for a Court to value saving owner’s equity (they have an uphill battle because the Court will be sceptical).

We explain the process involved below. We look at:

- Why would directors appoint a voluntary administrator at the 11th hour?

- How does court liquidation occur?

- The test set out in section section 440A(2) of the Corporations Act 2001 (Cth)

- Relevant case law: Weriton Finance Pty Ltd v PNR Pty Ltd [2012] NSWSC 1402, Re Laguna Australia Airport Pty Ltd [2013] FCA 1271. Re Offshore & Ocean Engineering Pty Ltd [2012] NSWSC 1296, Lubavitch Mazal Pty Ltd v Yeshiva Properties No 1 Pty Ltd (2003) 47 ACSR 197, Deputy Commissioner of Taxation v QBridge Pty Ltd [2008] FCA 1300.

Overall, it matters less when and in what circumstances the voluntary administrator was appointed, and more whether the creditors are better served by the administration or by a liquidation; this is what will affect the judge’s decision to grant a winding up application.

Why appoint a voluntary administrator?

The appointment of a voluntary administrator is usually initiated by the director seeking to save their company. It provides a moratorium from creditor action which allows the company to restructure without creditor interference (other than via a winding up application). The optional outcome for directors is a compromise through a DOCA that reduces the company’s debts. If the voluntary administration leads to the successful outcome of a DOCA, the directors will be given back their powers and allowed time to try and bring the company back to long term profitability and sustainability.

Why appoint a voluntary administrator at the 11th hour?

The 11th hour for a company is the time immediately before a Court date is listed for a compulsory winding up. The creditors (such as the ATO) have lost patience with directors and believe their interests are best protected by winding up, rather than waiting for the directors to straighten things out through a voluntary administration. This is a scenario where the creditors oppose an adjournment of the winding up process.

Appointing a voluntary administrator at the 11th hour is more than likely a last-ditch attempt by directors to delay a liquidation which would result in the death of their business. While a liquidation spells the end of a company, a successful DOCA arising from a voluntary administration will allow directors to return to trade.

How does court liquidation occur?

An application for an order to wind up a company can be taken to court (Federal or Supreme) to be heard by a Judge or Registrar. If the application is granted, the order for liquidation will be made and the Court will appoint a liquidator selected by the applicant creditor.

The legislation guiding a court’s decision

Section 440A(2) of the Corporations Act 2001 (Cth) provides that a Court must adjourn a hearing of an application for an order to wind up a company where that company is under administration, and the court is satisfied that it is in the interests of the company’s creditors for the company to continue with administration rather than be wound up.

This means that wherever there is an application to wind up a company (i.e. have it put in liquidation) and the company is currently undergoing voluntary administration, the Court must decide whether voluntary administration or liquidation would better serve the interests of the creditors – not the directors, or the business itself – in determining whether to wind up immediately.

The consequence of this legislation is that in any application for an order to wind up a company if the application is made by or on behalf of creditors who are primarily in support of the order, the directors and administrators must convince the Court that it is in the interests of creditors that the company not be wound up.

Application in case law

Recent case law applying s 440A of the Corporations Act 2001 (Cth) has supported a common-sense interpretation of the section in the following ways:

- For the Court to be required to grant an adjournment, it must be satisfied that it is in the creditors’ interests to continue the administration in all the circumstances, which involves there being a sufficient possibility – as distinct from mere optimistic speculation – that creditors’ interests will be accommodated to a greater degree in an administration than in a winding up (Weriton Finance Pty Ltd v PNR Pty Ltd [2012] NSWSC 1402 at [16] to [21])

- The defendant company (i.e. the voluntary administrator’s lawyers) bears the legal burden of satisfying the Court that an adjournment should be granted (Re Laguna Australia Airport Pty Ltd [2013] FCA 1271 at [11])

- A substantial degree of persuasion that administration rather than liquidation is in the best interests of the company’s creditors is necessary. This means proof is actually required (Re Offshore & Ocean Engineering Pty Ltd [2012] NSWSC 1296 at [6])

And, most relevantly:

- The Court will view with scepticism the appointment of administrators at the last minute in the face of winding up proceedings (Re Offshore & Ocean Engineering Pty Ltd (supra) at [16])

In weighing the issue of how and who can determine whether administration or liquidation best serves the interests of creditors:

- “Particularly in the case where commercial judgments may differ, there is force in the view that creditors are the best judges of their own best interests… But while I regard the opinion of an insolvency practitioner in this respect as relevant, ultimately it is for the judgment of the Court whether the continuation of the administration, as opposed to an immediate winding up, is in the interests of creditors.” (Re Offshore & Ocean Engineering Pty Ltd)

- “It may be said, why should this decision not be left to the creditors?… the overwhelming majority of whom have indicated a disposition in favour of adjourning the application to permit them to consider the DOCA. However, they have not been presented… with the fundamental truth… Ultimately the Court has to be satisfied that it is in the best interests of creditors.” (Re Offshore & Ocean Engineering Pty Ltd)

In summary:

- For an application to be rejected, there must be a sufficient possibility that administration will accommodate the creditor’s interest to a greater degree than liquidation

- The defendant company (being the directors and administrators) bears the burden of proof for establishing why an application should be granted

- There must be substantially persuasive evidence that administration would be better than liquidation for the administration to be allowed to continue

- The Court will likely look at an 11th hour appointment of a voluntary administrator as a negative reflection on the efficacy and value of administration over liquidation

- Ultimately, while the opinions of creditors and insolvency practitioners will be considered, the determination of what is in the creditors ‘best interests’ and how those interests will best be served is left to the interpretation of the judge

Further examples

- Lubavitch Mazal Pty Ltd v Yeshiva Properties No 1 Pty Ltd (2003) 47 ACSR 197

This case concerned an application for an adjournment of proceedings to wind up a company which had (very recently) been put into voluntary administration. The judge allowed the application in part, deciding that the appointment of the provisional liquidator would be preferable to salvage as much of the company as possible (and more could be salvaged through liquidation than through voluntary administration).

“On the evidence there was no prospect that a proposal might emerge for a deed of company arrangement that would produce a larger or accelerated dividend for the creditors than in a winding up. The evidence to the contrary was no more than optimistic speculation. For the same reasons CA s 440A(3) did not preclude the appointment of a provisional liquidator.”

“Section 440D of the Corporations Act 2001 (Cth) states that during the administration of a company, a proceeding against the company cannot be begun or proceeded with except with the administrator’s written consent, or the leave of the court.”

This case shows that provisional liquidators can and will be appointed by the court over the top of an 11th hour voluntary administrator.

- Deputy Commissioner of Taxation v QBridge Pty Ltd [2008] FCA 1300

This case concerned winding up proceedings before the court. Immediately prior to the commencement proceedings (at quite literally the 11th hour), voluntary administrators were appointed. Here, Greenwood J held the following:

“Accordingly, what I propose to do this. I will grant the adjournment of the application for the winding up order for, in effect, a period of eight days by which time the voluntary administrators will have had an opportunity to determine whether the amount of $100,000 is paid tomorrow and, secondly, whether, based upon their expertise and experience generally, the responses that they obtain from St George and/or Downer EDI leads them to believe that there is any prospect of a Deed of Company Arrangement emerging which would result in a dividend to creditors greater than a dividend upon liquidation or whether there is a prospect of a sale of the business either at an amount which would discharge the creditors in total as is suggested or at some lesser amount which would result in a calculation of a dividend which might be favourably compared with that obtaining in a liquidation.”

This decision shows that while the court is, in favourable circumstances, willing to maintain last minute voluntary administration appointments, they will still be treated with a degree of scepticism, and (as was the case here) liquidation will not be entirely ruled out, but rather put aside for a second return date.

Key takeaways

- Voluntary administration will always lead to either a deed of company arrangement or a liquidation anyway

- It is not the priority of the Court to ‘save’ a business (only to protect creditors)

- Courts will likely make a prima facie judgment (or a ‘smell’ test) of whether the voluntary administration seems beneficial or not very quickly

- Overall, it matters less when and in what circumstances the voluntary administrator was appointed, and more whether the creditors are better served by the administration or by a liquidation; this is what will affect the judge’s decision to grant a winding up application.

9. Conclusion of part 2

If considering liquidation, the first important factor to note is that the return for unsecured creditors is usually very small. In most cases, there is no return. It is possible that the new simplified liquidation process could result in better returns for the creditors of small businesses, however, there is little evidence of that to date.

Once directors think that insolvency is a possibility, they need to prepare for the possibility of liquidation and other formal insolvency processes. We set out the steps directors need to take in assessing their books and evaluating their liability before initiating a formal insolvency process.

Once the decision to go into liquidation has been made, directors need to ensure they choose the right liquidator. We set out key factors in making this decision including the size of the liquidator firm, their culture, price, experience and ethics.

Finally, we considered the possibility of directors appointing a ‘11th hour’ voluntary administrator to prevent imminent liquidation. Both the Corporations Act 2001 (Cth) and significant case law confirm that the courts will only allow this to occur where an applicant can prove it will be in the best interests of creditors (not directors, or the business itself).

In the next and final part of this Ultimate Guide to Liquidation, part 3, we will consider how directors and creditors can respond to liquidation. This includes setting out how liquidators can be replaced, how their conduct can be reviewed, and how businesses can best manage the fallout of a liquidation.

Part 3: Responding to Liquidation

1. Introduction

In part one, we considered the question ‘What is liquidation?’. We explained all the main types of liquidation in Australia (members’ voluntary liquidation, creditors’ voluntary liquidation and simplified liquidation), and briefly looked at some of the alternatives that are available (such as the safe harbour and restructuring under the Corporations Act 2001 (Cth)).

In this part, part 2, we look at how to prepare for liquidation. We begin by looking in greater depth at the shortcomings of liquidation (the returns for creditors are generally very low), before looking at general steps directors can take to prepare for liquidation, how to choose the right liquidator, and how the court will deal with attempts of directors to prevent winding up with the appointment of an ‘11th hour’ voluntary administrator.

In the next part, part 3, we will look at how businesses can best deal with the aftermath of liquidation.

2. Unsecured creditor prospects in liquidation

In liquidation, the company is wound up, any remaining assets are realised and distributed to creditors. But who gets priority for the remaining assets? Priority for the proceeds of the winding-up goes to secured creditors. Even among secured creditors, some interests, such as a Purchase Money Security Interest (‘PMSI’) have ‘super-priority’ over other secured interests.

For unsecured creditors, creditors who do not have a registered security interest in the assets of the company, funds are distributed in order of priority as set out in section 556 of the Corporations Act 2001 (Cth):

- The costs and expense of the liquidation, including liquidators’ fees;

- Outstanding employee wages and superannuation;

- Outstanding employee leave of absence (including annual leave and long service leave);

- Employee retrenchment pay;

- Remaining unsecured creditors.

Given the order or priority, what are the prospects of the remaining unsecured creditors getting a return? While there is frustratingly little recent data on the average return of insolvency for unsecured creditors, when Parliament looked into this in 2023:

- Personal bankruptcy statistics indicated average returns for unsecured creditors. at 1.6 cents in the dollar. We can assume that corporate insolvency is not much better;

- The dividend to creditors was estimated to be zero cents per dollar for 85 to 92 per cent of reported liquidations over the previous 15 years

Note also that these statistics overstate the prospect of a return for the median creditor. Outcomes are skewed by a few larger businesses leaving more significant pay-outs. In our experience, the expected return for the median unsecured creditor is zero cents on the dollar. As the overwhelming majority of windings up end up in Australia are small-sized and family businesses with a small asset base, it is unsurprising that zero assets are leftover in so many cases.

It is also worth observing that the financial loss from liquidations is not just a loss to individual creditors but constitutes a significant loss to taxpayers as well; the Australian Tax Office (ATO) is almost always the largest unsecured creditor and yet they have no priority and so are usually unable to recover unpaid taxes.

Several years ago, the Australian Small Business and Family Enterprise Ombudsman conducted an inquiry into the effect of insolvency practices on small businesses and made a range of recommendations. You can read more about it here.